Energy Musings contains articles and analyses dealing with important issues and developments within the energy industry, including historical perspective, with potentially significant implications for executives planning their companies’ future. While published every two weeks, events and travel may alter that schedule. I welcome your comments and observations. Allen Brooks

March 8, 2022

Offshore Wind And Its Version Of The Shale Land-Grab

BOEM held a sale for offshore wind leases off New York and New Jersey that set a record in high bids. The cost per acre and per MW reminded us of the land-grab frenzy of the shale boom. READ MORE

We Need A Neck Brace After Germany’s Energy Whiplash

Germany’s three-decade philosophy about how to deal with Russia led to tolerance and economic dependence. That philosophy was reversed in one speech, but what does it mean? READ MORE

Petroleum Is More Important In Our Lives Than Many Think

We show you two lists of critical items and everyday products we depend on that are made from petroleum. Many of them have no alternatives, showing our dependence on oil and gas. READ MORE

Thoughts On Random Energy Topics

Europe’s Infatuation With Heat Pumps Has A Long Way To Go

At 1% penetration rates, it will take years to make a dent in fossil fuel demand.

A Blow To Renewable Power In Germany Confirms Market Disruption

A wind turbine blade manufacturer to shut production due to auction impact on prices.

1970s Energy Crisis Playbook Is Being Resurrected

Windfall profits taxes and other 1970s rules and policies are being considered.

The Energy Super-Cycle Is Rewarding Investors In The Sector

Updated S&P 500 sector performance chart shows energy’s outperformance.

Offshore Wind Is Taking Its Lumps

Scotland’s lack of jobs; NJ’s lease sale delay; MA to revamp terms to hurt consumers.

Offshore Wind And Its Version Of The Shale Land-Grab

An auction process that spanned a three-day period in late February resulted in offshore wind developers bidding an amazing $4.37 billion for 488,201 acres of leases in the Atlantic Ocean off the coast of New York and New Jersey for new wind farms. These leases are projected to enable the winning developers to install potentially as much as 6,000 megawatts (MW) of offshore wind generating capacity, involving upwards of 500 wind turbines. This auction is a major step down the path laid out by the Biden administration for installing 30,000 MW of offshore wind capacity by 2030, as part of the government’s effort to totally decarbonize the U.S. economy by 2050.

Exhibit 1. Is This What Offshore New York And New Jersey Will Look Like?

Source: hydrosphere.co.uk

Newspaper and clean energy website headlines proclaimed that the auction’s results demonstrated that the clean energy revolution was firmly established. The lease results, which were reported in a Bureau of Ocean Energy Management (BOEM) release, show how the 63 bidding rounds resulted in steadily escalating bids for each of the six lease areas. What was interesting about the auction was that the winning bidders are all limited liability companies, mostly partnerships of European offshore wind developers and European energy companies. In fact, there was only one all-American partnership among the winning bidders, which is notable with regards to the efforts to build an American offshore wind industry.

The provisional winning bidders and their owners were:

OW Ocean Winds East, LLC – EDP Renewables (Spain) and Engie (France)

Attentive Energy LLC – EnBW (Germany) and TotalEnergies (France)

Bight Wind Holdings, LLC – RWE Renewables (Germany) and National Grid (UK)

Atlantic Shores Offshore Wind Bight, LLC – Shell (UK) and EDF Renewables (France)

Invenergy Wind Offshore LLC – Invenergy (US) and energyRe (US)

Mid-Atlantic Offshore Wind LLC ‒ Copenhagen Infrastructure Partners (Denmark)

We assume the bids will be accepted and the respective groups will complete their bid requirements and receive their leases. The process is likely to take several weeks to complete, but given the significance of this auction, let alone the amount of money BOEM is raising, it should move forward expeditiously. Then the serious work begins, as the lease holders must start working on selling their potential power output, along with engineering the projects, securing equipment supplier bids and lining up the logistics for installing the wind turbines and laying the cables to bring the electricity to onshore power markets.

The media was laudatory in its assessment of the sale’s results. Here are some of the headlines of stories reporting on the auction and the amount of money raised from the winning bidders:

Offshore wind lease sale nets record $4.4B – YAHOO News

New York Bight Lease Sale for Six Offshore Wind Energy Sites Raises Record Bids – NRG Wind Project

Biden-Harris Administration Sets Offshore Energy Records with $4.37 Billion in Winning Bids for Wind Sale – Electric Energy Online

A bight-sized sale rakes in more than $4B – Politico

New York Bight Offshore Wind Lease Auction Smashes Record ‒ gcaptain.com

One of the more significant headlines came from Grist, an online publishing organization that depends on donations to support their work. The headline read: “A record-breaking offshore wind lease sale signals a new era for development.” The more telling question was the sub-headline that asked the question: “But will more expensive leases mean higher electricity prices?” The residents of New York and New Jersey must be wondering the same thing, as their leaders have been executing a clean energy strategy that has boosted the cost of electricity for ratepayers. Will the next stage of their “green revolution” result in even higher power bills? Moreover, what can ratepayers do about it if that is the likely outcome? We will come back to some of the key points raised in the Grist article, but first some of our reactions to the news.

Our first reaction to the bidding results was that this was a highly significant event for the offshore wind industry, as well as for the renewable energy business. In fact, it may be as significant as what happened following the first area-wide Gulf of Mexico oil and gas lease sale in May 1983 was to the offshore drilling business. We are a few months short of the 39-year anniversary of that sale, and we doubt many people remember it or its significance for the offshore industry and ultimately U.S. oil and gas production.

Prior to the Department of the Interior’s revision of offshore oil and gas leasing, every block put up for auction had to be nominated by at least two oil companies. That process was designed to ensure that there would be bidding on the leases offered for sale. However, this required oil companies to collaborate with their competitors and could result in company exploration strategies being revealed as they sought support for lease nominations.

After a lengthy process to reassess the goals of federal acreage leasing, considering the explosion in oil prices during the 1970s and the realization that domestic oil and gas output was in a terminal decline, the idea emerged to unshackle the industry in its pursuit of new acreage to drill. The downside to this strategy was that the government risked selling substantial amounts of acreage for the minimum bid price established by the U.S. Geological Survey’s assessment of potential reserves and their value for each lease. Competitive bidding generally resulted in the government earning more money from a sale than was envisioned by the area-wide concept.

The upside to the lease sale design switch was that more companies could acquire acreage cheaper and thus it might stimulate drilling and result in a reversal of the decline in domestic oil and gas output. The offshoot to that theory was that companies that could acquire cheap acreage might be willing to test radically different geological interpretations of the sediments offshore with even greater long-term positive outcomes. They could test these theories, while at the same time assembling blocks of acreage that might cover an entire new field, providing an incentive to bid and drill. They also could test their theories without having to disclose them to competitors to gain support for getting a block nominated under the former lease sale structure.

The May 25, 1983, Central Gulf of Mexico Sale 72 was a smashing success and marked a significant inflection point for the U.S. oil and gas industry. A record $4.58 billion was bid on 656 leases by 80 companies. The total of accepted winning bids on 623 tracts, totaling 3,089,872 acres, was $3.37 billion, the most money ever raised in a lease sale. Combined with the next three area-wide lease sales, the oil and gas industry acquired over eight million acres. There was an almost immediate recovery in offshore drilling activity as rigs were contracted and drilling commenced. The industry recovery, unfortunately, was cut short by the OPEC oil war that had already commenced but became more visible and contentious in 1984 and peaked in 1985 with the collapse in global oil prices to $10 a barrel.

One of the more interesting events to emerge from Sale 72 was the immediate declaration of a new commercial field from an oil company that had previously drilled a dry hole when oil prices were lower, making the discovery non-commercial. They relinquished the tract. The area-wide sale permitted them to reacquire the tract and upon approval of their bid, the company was able to declare a new discovery and a development plan because higher oil prices made it commercial.

The record for high bids was surpassed in 2008 with the Central Gulf of Mexico Sale 206 when the industry offered 1,057 bids from 85 companies on 615 tracts resulting in $3.68 billion wagered. This record sale was driven by global crude oil prices above $100 per barrel, with expectations that with the surge in demand driven by China there was no end to rising global oil demand. Once again, much how the 1970s high oil prices changed the trajectory of the oil industry in the 1980s, the perceived trajectory of the oil and gas industry in the 2000s was altered by the earlier years of high oil prices. Because the offshore industry offered one of the largest unexplored regions of the world, it was not surprising that there was significant attention being paid to this sector at the executive levels of oil and gas companies in the 2000s.

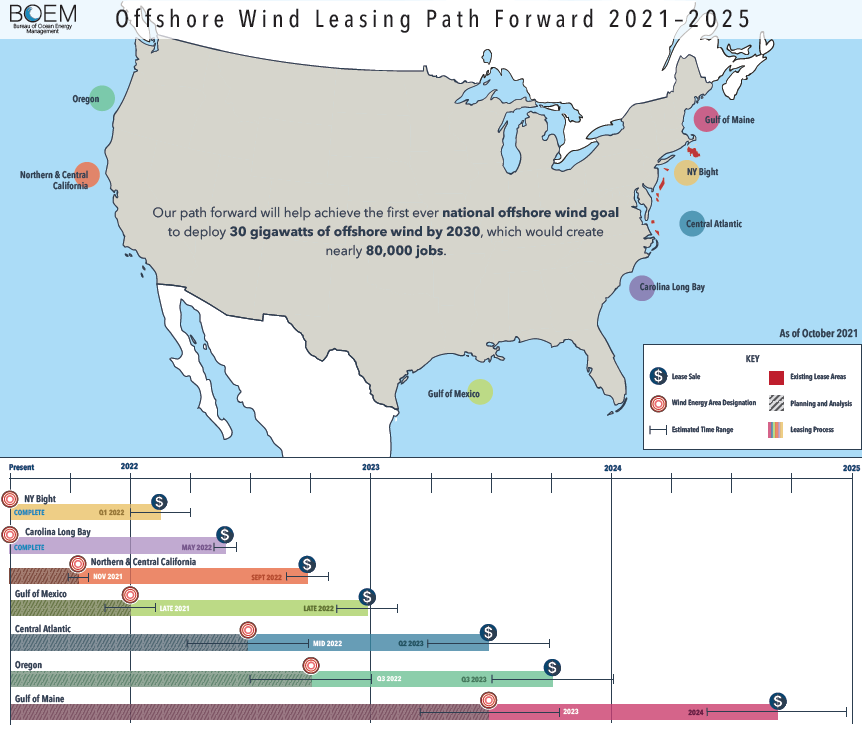

The New York Bight wind lease sale is a key component of the Biden administration’s offshore leasing plan. The chart below shows the offshore wind energy path being established by BOEM. It highlights the areas off the east and west coasts of the country targeted for offshore wind farms. Below the map are timelines for each of the developments, as the Biden administration is aiming for having 30 gigawatts (GW) of offshore wind power by 2030. According to some estimates we have seen, the goal will be met by combining the total of actual offshore wind generating capacity installed by that date plus the amount of wind capacity that will be under development.

Exhibit 2. The Biden Administration Plan For Offshore Wind Energy

Source: BOEM

Before discussing the state of the offshore wind industry, we wish to address the euphoria surrounding the Bight lease sale results. Almost every headline during the auction, especially those during the early bidding rounds, focused on the ever-increasing amounts of money being bid. The rising totals reflect how much green energy, and offshore wind is clearly one component, is favored by lenders and capital providers. While the $4.37 billion lease bonuses wagered is a record, it should be put into historical perspective.

Central Gulf of Mexico Sale 70 raised $3.4 billion in 1983, while the record Sale 206 in 2008 hit $3.7 billion. In 2022 dollars, Sale 70 was worth $9.7 billion, while Sale 206 yielded high bids of $4.8 billion. Yes, the times were different and industry conditions were different, but it is always good to pause and assess the significance of developments for an industry.

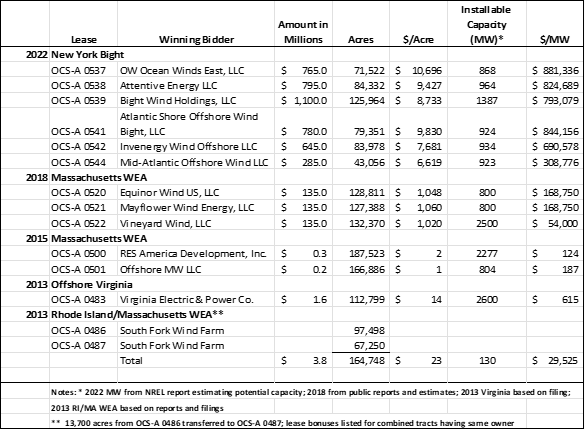

We have prepared a table (below) showing the results of the recent offshore wind lease sale, along with selected other lease sales. Our focus is on the amount of money bid, the number of acres in the lease, and the amount of generating capacity targeted for each lease. Because there are no specific projects for the leases at the time they are acquired, the generating capacity estimates often come from the National Renewable Energy Laboratory (NREL) based on assumptions about average wind speed, turbine size and capacity rates. In our table, we also calculate the bonus paid per acre and the cost per MW of the estimated generating capacity for the lease. We have gathered similar data for sales from 2018, 2015, and 2013, and in some cases details about the development plans are public. What is also meaningful when looking at the recent lease sale is to note that BOEM reported that through the 2015 Massachusetts lease sale it had leased competitively about 700,000 acres for offshore wind farms and received $14.5 million in lease bonuses. That translates into $20.71 per acre leased. Since we do not have specific acreages for some of the early leases and estimated generation capacity figures, we cannot calculate comparable amounts spent per acre or per MW for these leases, beyond those we have included in our table.

In the table, we draw your attention to the magnitude of the bid amounts per acre and per MW of installed generating capacity for the recent sale compared to the results from earlier sales. Two earlier sales stand out for how ridiculously low their bid figures were.

Exhibit 3. New York Bight Wind Lease Sale Results Plus Other Auctions

Source: BOEM, PPHB

The 2015 Massachusetts WEA sale of OCS-A 0500 and OCS-A 0501 likely reflect the location of the leases. There were two additional tracts included in that sale that received no bids. All the tracts are in Nantucket Sound near where the earlier proposed Cape Wind project was targeted to be built. For readers not familiar with Cape Wind, it was the first proposed offshore wind farm, and it became a lightning rod for opposition from wealthy and politically connected residents on Nantucket and Martha’s Vineyard as well as on Cape Cod who were opposed to seeing wind turbines on the horizon from their summer homes. The sponsors of the project labored under intense opposition, a series of legal challenges, technical issues with the radar claimed by the military that has a strong presence in the region, struggles to secure financing, and a whole host of other less onerous but time-consuming issues. After 10-years of battle and a cost that was escalating to levels that made the project uneconomic, the sponsors pulled the plug on Cape Wind. Given that history, it is not surprising that bidders for nearby leases would be hesitant about waging much money on what might become another multi-year quagmire and financial black hole.

When we look at the 2018 Massachusetts lease sale, we see per acre bids in the $1,050 range and the cost per MW of almost $169,000, except for lease OCS-A 0522. We are not sure about how many MW of generating capacity can be installed, but the press release discussing the results of the sale gave a figure of 4,100 MW for all three tracts. We know from filings that the first two sites are targeting 800 MW each, so that leaves an estimated 2,500 MW for Vineyard Wind’s project on the third site.

If we compare the figures for the 2018 sale with the recent Bight sale, there has been a quantum leap in amounts of money developers are willing to spend to secure leases. Based on the cost per MW of generating capacity, for the recent sales to get close to the estimates for the 2018 Massachusetts sale, roughly four to four and a half times the generating capacity would need to be installed. That is not a likely scenario.

What the reporter for Grist commented on in his article was that once the wind farm developers begin negotiating their power purchase agreements (PPA) with the electric utilities, the issue will become how expensive this power might be. Of all the media we read about the results of the wind lease sale, we found only the Grist reporter questioning the economic rationale of the huge bids. He wrote the following based on a conversation with a wind energy observer.

Willett Kempton, associate director for the University of Delaware’s Center for Research in Wind, said higher electricity prices are possible, but the effect would likely be small — he estimates the unexpectedly high lease bids could result in power costing roughly 20 percent more than it otherwise would. But at the same time, he noted that the costs of development are still declining and that competition among wind companies to win contracts with states like New York and New Jersey could also exert downward pressure on electricity rates.

We guess his “20 percent more” cost estimate was already factoring in the declining trend in development costs, as that is a standard assumption among wind energy proponents. We wonder if they have updated their thinking based on wind turbine manufacturers raising prices and acknowledging that costs are not likely to decline for the foreseeable future?

Further to the economic issue, the Grist reporter interviewed Fred Zalcman, director of the New York Offshore Wind Alliance, an industry advocacy group, who said he thought it was too early to know what impact the bids might have on ratepayer bills. Of course, he does not want to throw any cold water on his group’s wild party. He pointed to the continued improvement in turbine efficiency and the growing domestic supply chain for offshore wind that should help bring down development costs. It should be noted, however, that this supply chain is largely non-existent, currently, but it is targeted to receive money and incentives from local governments fighting to become the center of the offshore wind business.

Zalcman also commented that the high lease prices really reflect a mismatch between demand for offshore wind energy and the supply of lease areas. He was quoted stating: “I think if we develop more lease areas, that will help relieve some of the upward pressure on these lease prices.” This view was echoed by a wind analyst at energy consultant Wood Mackenzie who agreed that the bid prices reflected the view of offshore wind developers and investors of the existence of a sound business case for offshore wind in the U.S. On the other hand, we question how much of the bidding activity was driven by the fact that in the last major offshore wind lease auction in the U.K., no traditional wind developer secured a lease, as international oil companies, keen on burnishing their clean energy transition image, outbid them. Those traditional offshore wind farm developers were quite active in this sale, although there were a couple who partnered with international oil companies.

We also found it interesting that Chelsea Jean-Michel, a wind industry analyst at Bloomberg New Energy Finance (BNEF), a huge clean energy sponsor, told E&E News that the earliest she expects the new projects to come online is 2030. That is eight years from now, and such a time lag will be very disappointing for the Biden administration, much less the ratepayers in New York and New Jersey who are facing power supply shortages as nuclear and fossil fuel power plants in those states are shut down. Such a long time for these new wind farms to start up will play havoc with New York and New Jersey meeting their acclaimed clean energy targets.

Another perspective on the challenges the offshore wind farm business is facing came from an interview by Recharge, a clean energy web site, with Christina Aabo, who headed R&D for global offshore wind pioneer Ørsted for over a decade before recently stepping down to join a green energy consultancy. In her opinion, “We have a fundamentally sick industry.” Wow! That is a stark verdict but supported by the problems she sees from the business models of wind turbine manufacturers, the surge in non-traditional developers, aka, the international oil and gas companies, who lack senior people so leave it to junior executives to make decisions on a “trial by error” basis, and the never-ending push for cheaper and cheaper power.

In her view, “Developers are competing so fiercely, bidding down, down, down. We had the cost of electricity so fiercely in our DNA we forgot to look to anything else. We were so eager on getting the curve down we forgot to take a pause and let it flatten out. We will see that it’s going to kill part of the supply chain.” She believes this will lead bankruptcies among suppliers who have been investing so much in pushing the envelope of wind turbine technology that they have lost sight of how to make money.

For Aabo, the offshore wind industry must come to an understanding with society that the price of electricity is not the only measure of energy’s value. She says developers need to promote their power for its sustainability, technical innovation, industrial benefits, or contribution to energy security, and not merely its price. For green energy promoters, such a discussion is not needed because the “science is settled.” Such a discussion, however, is exactly what the fossil fuel industry is demanding as it is being called upon to bail out the failed experiments with intermittent green energy. Aabo, a long-time veteran of the offshore wind industry, is acknowledging the reality that wind energy has a role to play, but that role is not exclusive and needs to be better defined. While she did not say it in the interview, we suspect she believes the future for offshore wind will still be bright even after having the industry’s role better defined. That is certainly a refreshing position.

As we followed the Bight lease auction and the rising dollar amounts bid, we began to wonder whether we were seeing offshore wind energy’s “shale land-grab moment?” We are not sure how many readers remember the early days of the shale revolution when the marriage of horizontal drilling with massive hydraulic fracturing of formations enabled the industry to tap large, previously unproducible natural gas resources and led to a surge in gas production. That technology was pioneered by George Mitchell at Mitchell Energy who was desperate to find new gas production to fulfill a long-term supply contract. The technology demonstrated its value when natural gas prices soared into double digits in 2005. Was the U.S. running out of natural gas once again? The industry made sure that would not happen. For good or bad, the gas shale boom created the liquefied natural gas (LNG) export business that is proving critical to helping Europe cope with its growing energy crisis and now the Russian-Ukraine fight.

The success of gas shale drilling spurred a land rush as companies, most prominently Chesapeake Energy, led by landman CEO Aubrey McClendon, raced across the countryside leasing up huge swaths of potential shale gas acreage before their competitors could. For a while, being a landman proved to be a lucrative job. Heretofore, they merely slaved away searching the land records in the bowels of county courthouses throughout the petroleum patch seeking to determine the ownership of mineral rights and perfecting the titles to those resources so they could be leased. Without more acreage, the shale revolution would have petered out.

The shale revolution – driven by technological successes and high gas prices – proved so prolific that the newly discovered output created a glut that drove gas prices to record lows. But the revolution was rejuvenated when the technology proved applicable to crude oil formations. This new effort kept the boom going – and likely propelled it to new heights.

Capitalizing on this new-found business model, companies competed aggressively to scoop up acreage before competitors, as the inventory of leases inflated the value of companies regardless of whether wells had been drilled or not. Cheap money from lenders and investors fueled the boom. The legitimacy of the shale revolution/boom was cemented with ExxonMobil’s agreement to buy shale leader XTO Energy for $31 billion in stock in 2009, equal to 10% of the company’s market value. The giant of the global petroleum industry had just endorsed this technology and its disruptive potential. ExxonMobil CEO Rex Tillerson, a production engineer by training, justified the deal and the price paid after admitting that his company had lacked the requisite shale technology within its E&P ranks, so buying a leading shale producer and assigning it the task of leading ExxonMobil in the shale revolution was critical for the company’s long-term success. ExxonMobil shareholders rued the day that transaction closed.

In reflecting on the land-grab experience that propelled the shale boom, we learned that buying high-priced leases with cheap money was a ticket to unprofitable outcomes. In fact, the leverage companies assumed to participate in the shale boom contributed to the petroleum industry generating the worst financial performance for a sector in the stock market for over a decade. The pain from this outcome, which cost people their jobs and investors their wealth, should not be forgotten. It is why “financial discipline” is such a watchword in the petroleum industry now. That does not mean to not invest in the business, but rather to weigh how much to invest while keeping balance sheets strong and investors happy with incremental returns. While we are not predicting it, the Bight wind lease sale euphoria suggests to us that a new group of energy players may be falling into the same trap shale oil and gas producers of the 2000s did. Will the results be the same? Who knows? What we do know is that history does not repeat, but it does rhyme.

We Need A Neck Brace After Germany’s Energy Whiplash

Up until February 24th, Germany’s energy and military policy rested on a clean energy future and limited spending for armaments. On that day Russia launched a comprehensive invasion of a former Soviet state, the independent nation of Ukraine. The invasion was not without plenty of warnings, as Russia had maintained troops along Ukraine’s border with Russia since the latter seized Ukraine’s Crimea region in 2014. During the latter months of 2021, Russia added to its military presence along the border and began war games, often in concert with its puppet regime in neighboring Belarus. This activity was seen as an implied threat against Ukraine seeking membership in the NATO alliance. When Ukraine continued to push for a date-certain for membership, the prospect of a military confrontation appeared certain.

The war between Russia and Ukraine brought into question this longstanding cooperative relationship that has existed between Russia and Germany. As a recent article in Foreign Affairs magazine by Sudha David-Wilip and Thomas Kleine-Brockhoff titled “A New Germany: How Putin’s Aggression Is Changing Berlin” pointed out, this relationship was based on “the ugly legacy of German military aggression during the twentieth century.” That legacy produced a mindset among Germans that “dialogue and multilateralism” were the key to peaceful coexistence and were “the only tools of foreign policy.” Therefore, developing a symbiotic relationship with Russia was seen as how best to deal with the latter’s military and economic pushes.

That policy of dialogue and multilateralism appears to have changed during a special Sunday session of the German parliament in the days immediately following the invasion of Ukraine. Olaf Scholz, the new chancellor, declared, “It is clear that we must invest much more in the security of our country, in order to protect our freedom and our democracy.”

That statement marked a dramatic transformation of Germany’s mindset. It would shed its reluctant and dovish foreign policy and commit to a significant increase in defense spending. Scholz’s government was deciding to isolate and punish Russia after decades of appeasing and accommodating it. This patience with Russia was born from a belief that there would be no peace on the European continent if Russia were shut out. That translated into the view that an economic interdependence would result in a steady relationship between the two countries. Remember that Germany is the largest economy in Europe and the titular head of the European Union. Germany’s policy toward Russia is akin to that of Bill Clinton’s when he said welcoming China into the World Trade Organization would lead to a more open and cooperative relationship between the western powers and China. It seems neither policy has worked.

For decades, the foreign policy position of Germany toward Russia required endless patience, even after Vladimir Putin’s aggressive speech at the Munich Security Conference in 2007, when he accused the United States of a monopolistic dominance in global relations. He claimed that the U.S.’s “almost uncontained hyper use of force in international relations” was destabilizing global security. He opposed plans for the U.S. missile shield in Europe proposed by President George W. Bush. Ten months after Putin’s Munich Speech, as it has been labeled, Russia suspended its participation in the Treaty on Conventional Armed Forces in Europe.

Germany continued to adhere to its dovish foreign policy despite Putin’s invasions of Georgia in 2008 and Ukraine in 2014. Germany led Europe’s push for sanctions on Russia following its annexation of Crimea and its incursion into Ukraine’s Donbas region. However, it counterbalanced that action with a push for greater economic cooperation represented by Germany’s offer to build the Nord Stream 2 natural gas pipeline in 2015.

For Germany, Russia’s invasion of Ukraine has changed everything – its foreign policy and economic cooperation policies that have lasted for three decades. Just how significant is this change? German Foreign Minister Annalena Baerbock said that “perhaps on this day, Germany is leaving behind a form of special and unique restraint in foreign and security policy.” That may be an understatement. That restraint had been the subject of pressure from NATO allies and Ukraine’s leaders for Germany to provide arms to fight the Russian invasion. The previous policy’s significance was explained at the Munich Security Conference in February when Baerbock pointed to the lessons from history in which supplying weapons to a region where German forces killed millions of citizens during World War II could only result in more guilt.

Germany’s Chancellor Scholz shocked the foreign policy community, the country, and even many in his own parliamentary party when he announced an immediate one-time investment of €100 ($113) billion in the Germany military. In addition, he declared the government’s intention to elevate defense spending to more than 2% of overall economic output – a goal set for NATO member states and pushed aggressively by President Donald Trump. Scholz indicated that Germany needed a fully modernized armed forces that did not need to borrow things from other units when deployed by NATO. He also indicated that buying American-made F-35 fighter jets is back on the table, and he committed to working with France and Spain to develop a sixth-generation fighter jet. Scholz also floated once controversial possibilities such as the use of armed drones and participation in NATO’s nuclear weapons sharing arrangements. This strategy reversal was backed by a statement from economically conservative Finance Minister Christian Lindner of the Free Democrat Party who said Germany will aim to turn its military “into one of the most capable, powerful and best equipped armed forces on the continent.” Such a statement not long ago would have led to Lindner being called a “warmonger.”

Equally as dramatic as the foreign and military policy shifts was the one for energy. It was necessitated by Scholz’s call for “a German diplomacy without naiveté.” No longer would the diplomacy involve Wandel durch Handel (change through trade). While Putin leads Russia, that foreign policy guideline will be a relic of the past. Germany is determined to deter Putin from his quest to change the balance of power in Europe. That calls for a new Germany energy policy, which will necessitate walking a fine line between the reality of fossil fuels and the goal of a decarbonized economy. To do it means developing new domestic energy sources while also weaning Germany off its Russian natural gas supply. Something easier said than done, at least in the near-term.

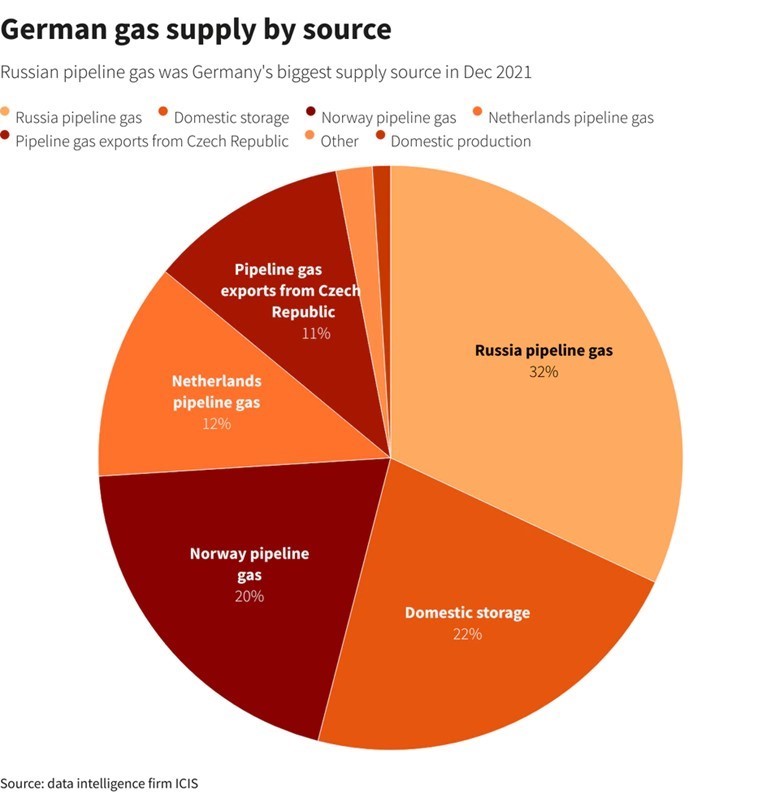

Russia supplies between 33-40% of Europe’s natural gas, depending on the month. In 2021, Germany imported 142 billion cubic meters (bcm) of gas, 6.4% below 2020’s use according to foreign trade statistics office BAFA. It does not identify where the imported gas originates. On the other hand, energy consultant ICIS shows in the chart below Russian pipelines providing 32% of Germany’s gas supply in December 2021, the largest market share.

Exhibit 4. Germany’s Natural Gas Supply Sources, December 2021

Source: Clean Energy Wire

Dr. Klaus-Dieter Maubach, CEO of German utility Uniper, last month pegged Russia’s share of Germany’s gas supply at half, although he acknowledged that this share fluctuates monthly. There is no denying that Russia natural gas is a critical component of Germany’s energy mix, especially given that Germany’s domestic gas production peaked in the 1990s and now only accounts for about 5% of the nation’s annual consumption. As a result of this dependency and with few alternative suppliers, Maubach commented that “Russia in its (gas supplier) role cannot be replaced during the next few years.”

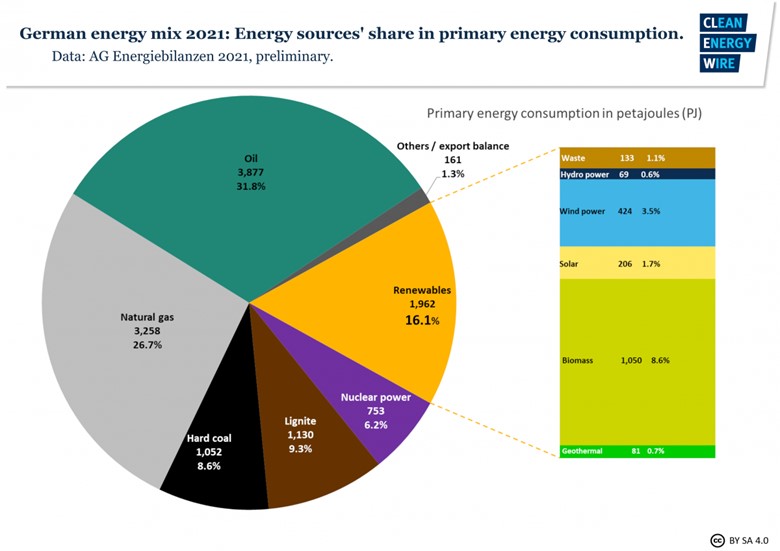

As the chart below shows, natural gas represented slightly more than a quarter of Germany’s primary energy consumption last year. That dependency is not likely to change much this year, even with high gas prices.

Exhibit 5. Germany’s Primary Energy By Fuel, 2021

One of the first energy steps Scholz proposed taking is for Germany to build two new liquefied natural gas (LNG) terminals that would allow alternative supplies to enter the country. One terminal would be located at the port of Brunsbüttel on the mouth of the Elbe river in the northern portion of Germany and in proximity to the Kiel Canal that would facilitate LNG distribution elsewhere in the country. The possibility of building this terminal was raised in 2018 and a tender was launched in 2019, but progress was slowed by opposition from environmental activists led by climate justice group Ende Gelände. The project had a price tag of €500 ($565) million in 2019, and is being developed by Gasunie, who issued a press release the day after Scholz’s speech saying negotiations were in “the final stages.” Gasunie hopes to begin construction of the terminal before the end of 2022, and the terminal is being designed to be able to import green hydrogen. A second terminal would be constructed to the west at Wilhelmshaven. Both sites are in northern Germany. LNG terminals usually require 13-14 months for construction once permits are in place, assuming there are no hiccups with equipment and construction.

Exhibit 6. Brunsbüttel Port And Kiel Canal

Source: militaryanalysis.blogspot.com

A second major policy change calls for the government to introduce a new law prescribing minimum levels for gas storage. Germany has 24 bcm of underground caverns for gas storage. A fifth of that capacity is owned by Rehden, a unit of storage company Astora, which is owned by Russian gas company Gazprom, a potentially complicating factor given government sanctions against Russian companies. Still, the volume of Germany’s gas storage is the largest available in central and western Europe.

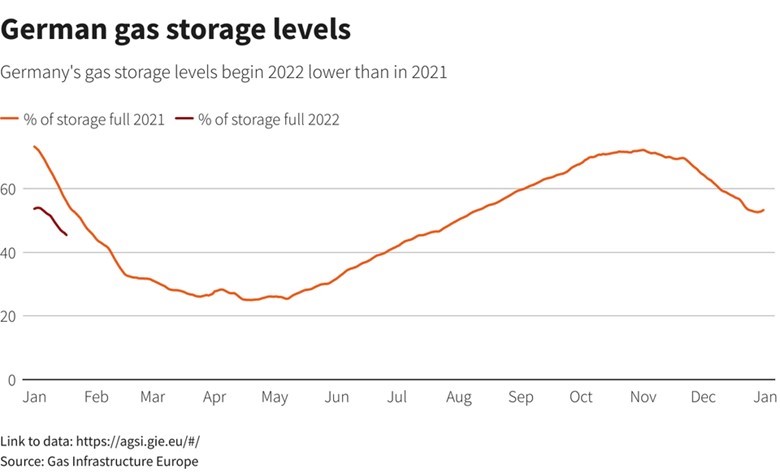

Exhibit 7. Germany’s Natural Gas Storage History 2021-2022

Source: Reuters

Despite a warmer winter, Germany’s storage caverns currently stand at only 30% full, according to industry group Gas Infrastructure Europe data, although the chart above reflects data from an earlier date. With the new law, Germany is proposing that gas storage capacity must be 65% full by the beginning of August and at 90% by December 1. We do not know what penalties might or will be assessed for companies not reaching those levels. We also do not know if the threshold is for each individual cavern or for the entire gas storage industry. The basic goal is for gas storage to supply Germany for 2-3 weeks of usage based on average temperatures during winter months.

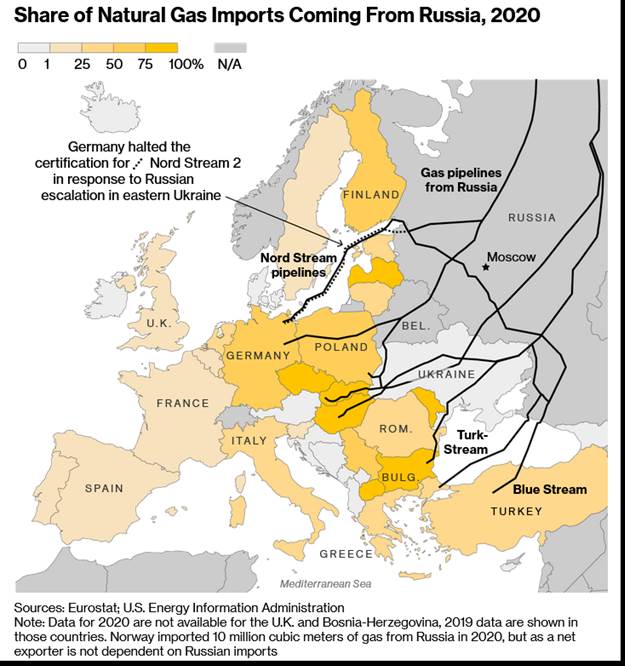

Another important energy market for Germany, which proved its importance last year, is coal. When Germany was forced to restart recently retired coal-fired power plants last year to keep its power grid functioning, the plants were sometimes hobbled by fuel supplies. Therefore, the government is working on a plan to mandate coal reserves sufficient to guarantee operation of coal plants for 30 days. Part of what is being discussed is where the coal inventory will be stored and what will be the possible sources. Russia has been a major supplier of coal to Germany. It is estimated that Russian coal accounted for roughly 45% of Germany’s imports last year. This dependency is below the radar screen given the intense focus on Russia’s natural gas supplies to Germany.

Exhibit 8. European Country Reliance On Russian Natural Gas In 2020

Source: Bloomberg

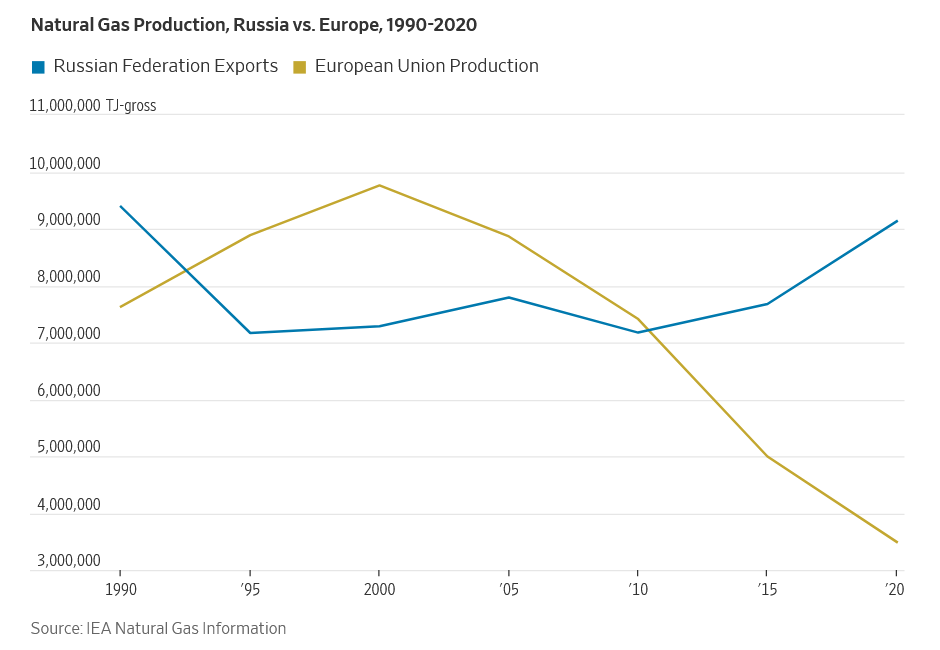

The chart above shows 2020 gas flows into European countries from Russia. The proximity of large volumes of gas supply from Russia that can be delivered by pipeline explains why Europe has embraced this energy source. Another reason for Russian dominance in supplying gas to Europe has been the decline in the continent’s domestic supplies. The chart below from the Wall Street Journal shows how Europe’s domestic gas output has declined and Russia’s exports have grown. This is not a reality driven by the absence of hydrocarbons in Europe, it was a political, economic, and policy choice. As they say, you make your bed and now you sleep in it.

Exhibit 9. Europe’s Gas Production Vs. Russian Gas Supplies

Source: Wall Street Journal

For the new German government, it spent the final months of 2021 organizing its new bureaucracy and prepping its governance plans. Those plans rested heavily on increased investment in renewable energy, and more rapid exits from fossil fuels – primarily coal and nuclear. Those plans were tested throughout 2021 and played a key role in the outcome of the German elections. The new coalition government has a meaningful representation from the Greens party, which will influence its stand on climate change policies, especially the accelerated push for net-zero carbon-emissions economy.

Therefore, the energy actions announced by Scholz must be viewed in the context of the continuing push to rid Germany of fossil fuels. The question is how quickly that transition may happen considering the need to protect consumers from the high cost of energy now and likely for the foreseeable future until all the “low cost” renewable power can be built.

To meet that challenge, the German government is proposing to extend the operating lives of its coal and nuclear power plants. This explains why the government is developing a coal fuel supply plan. Coal is targeted to be completely shut down before 2038, a date that has been scheduled to move forward to 2035 or earlier, if possible. Last December, under the long-established plan to phase out nuclear power, Germany shut down three of its remaining six operating nuclear plants, leaving the nation with 4.2 GW of nuclear generating capacity.

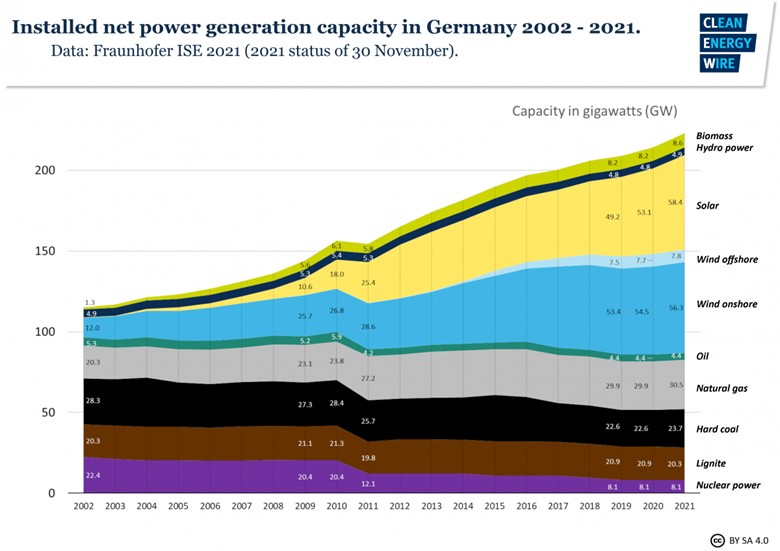

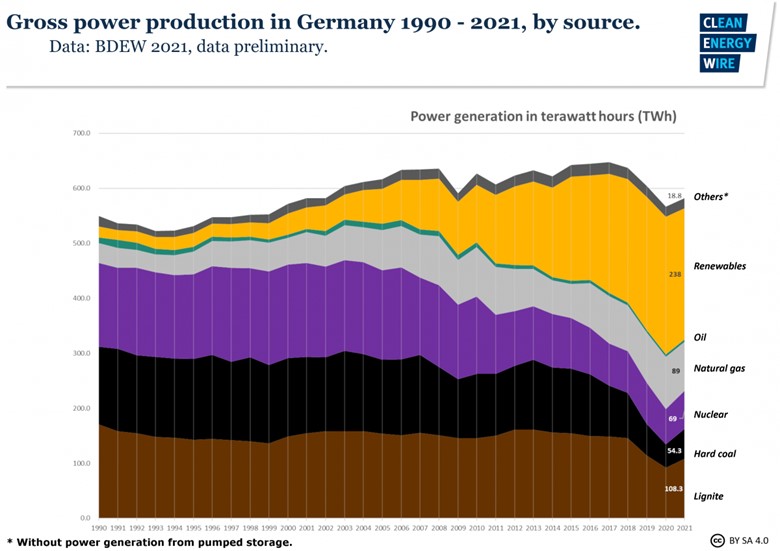

Before considering the legal and operational challenges of extending the lives of the three nuclear plants, we should examine the totality of Germany’s electricity generation situation. The following two charts show the status of Germany’s electricity generation capacity and its power output by fuel historically through 2021. If we consider which fuels are delivering above their capacity generation, there is no question it is fossil fuels, including nuclear. In 2021, coal represented 19.7% of Germany’s electric power capacity, but accounted for 28.2% of the power generated. Likewise, natural gas delivered 15.4% of the power generated while having only 13.7% of total capacity. Nuclear was the clear winner by producing 12.0% of the power generated but accounting for only 3.6% of capacity. All renewables (wind, solar, hydro, and biomass) represented 61.0% of total installed generating capacity, but only produced 41.2% of the power. This speaks to the weakness of intermittent renewable energy.

Exhibit 10. Germany’s Power Generation Capacity By Fuel Source

Exhibit 11. The History Of German Power Generation By Fuel Source

Source: Clean Energy Wire

After shutting down the three nuclear plants at year-end, Germany has 4.2 GW of operating nuclear generation remaining, or approximately 2% of the nation’s adjusted generation capacity, excluding any new renewable power installed in the first two months of 2022. If we assume that the remaining operating nuclear plants produce the same 3.3 times their capacity in power as nuclear did last year, then these three plants could account for roughly 6% of the electricity generated this year, assuming power generated remains flat with 2021. Is it worth having those nuclear plants operating? We would say yes. Is it possible? Let’s see.

Under current legislation, the operators lose the right to operate the remaining plants beyond December 31, 2022. If the network regulator, which is a part of the Economy Ministry, decided these plants are critical to Germany’s security of supply, it could allow them to run longer, which they are technically capable of doing. This, however, would require parliament to change existing laws, most notably the 2017 law that had the utilities transfer their decommissioning funds to a public trust.

Politically, this will be contentious issue. The minister for nuclear safety, a member of the Greens party, said last week that such a move was irresponsible and unsafe. His boss, Economic Minister Robert Habeck said that while there would be no taboos when looking into supply security, the idea of using imported coal for longer or letting existing nuclear plants remain online were unlikely to be feasible solutions.

Moreover, the plant operators have pointed out challenges they would face with a decision to extend plant operations. Given the legislation, they have been working toward the decommissioning timetable, so they would not have the staffs nor the fuel to continue to operate the plants. One operator was open to the idea of working to overcome these hurdles if the government determined continuing the plant’s operation was critical. The other operator was less receptive to this idea. So, what are the odds of these plants operating in 2023? We would guess less than 50%, but we never underestimate the power of governments to make things happen if they want them to happen.

The most important question, and one that cannot be answered, is how much of the rhetoric and policy moves will be sustained once the Russia-Ukraine war ends and potentially Putin leaves the world stage? As opinion writer George Will penned in his column in The Washington Post last week about the “180-degree turn” in German foreign and economic policy:

The physics of international politics sometimes tidily illustrate Newton’s third law of motion: When two bodies interact, their forces on each other are equal in magnitude and opposite in direction. Vladimir Putin’s war has provoked opposite forces of more than equal magnitude.

How would a new leadership in Russia deal with the west, and in particular Germany? This is a critical question given the many political contortions Germany has undergone in sustaining its strong economic ties with Russia, primarily through its reliance on that nation’s fossil fuels to ensure Germany’s industrial power. What would be the fate of the completed but uncertified Nord Stream 2 natural gas pipeline connecting the two countries? Will the weaknesses of renewable energy, and the reality of their costs for German households and businesses, produce a permanent change in the nation’s green energy agenda or will the politicians revert to the agendas the leaders were elected on last year? The power of the Greens party cannot be underestimated for driving the green energy agenda once the war is over.

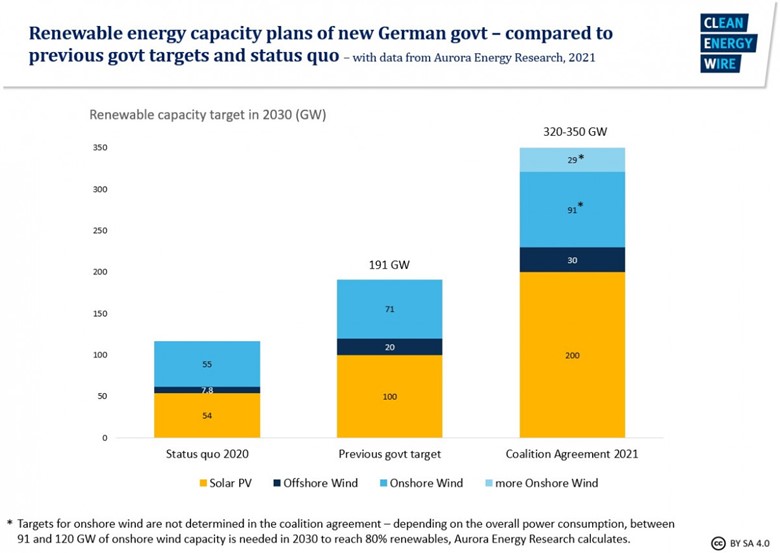

The chart below shows Germany’s renewable energy plan as of last year. How will the new energy focus alter the plans of developers in meeting this plan, or is the plan even open to revision? Can the country continue along this green energy path, while also fulfilling the new commitments pledged by Scholz in his Sunday speech?

Exhibit 12. Germany’s Plan For A Renewable Energy Future

Source: Clean Energy Wire

As much as we would like to believe Germany realizes that the problems it confronted with its green energy strategy last year will force adjustments, we are not convinced any deviation will be sustained. The verdict will only begin to become clear once the German public confronts the cost of the green energy strategy, increased military spending, and the need for a more diverse energy supply mix in the near-term. Watching what unfolds in Germany over the balance of this year, depending on how the Russia-Ukraine situation is resolved, will tell us much about Europe’s energy and economic future. That, in turn, may provide a template for energy policy in this country. We are not optimistic the green energy wave will be stopped, but it may be slowed.

Petroleum Is More Important In Our Lives Than Many Think

It is popular among climate activists to preach that society needs to leave fossil fuels in the ground and immediately switch to powering our economy with renewables. This view is laughable because it has no relationship to the reality of modern economies and societies. Yes, we release CO2 into the atmosphere when we use fossil fuels, but we also produce significant individual and societal benefits. The activists never acknowledge those benefits and that is a failing in their argument.

The producers and users of fossil fuel-generated energy must be cognizant of their carbon emissions and strive to limit them. Even little things like turning off lights and lowering thermostat temperatures to use less heat and electricity is a step in the right direction. One of the problems is that many of our household appliances are always on because they are designed to respond instantly to our desire to use them.

Planning the most efficient route when driving for errands is a fuel and sometimes a time saver. UPS drivers are famous for planning their delivery routes, so they do not make left-hand turns that often require idling while awaiting a break in the traffic traveling in the opposite direction. UPS does this to save time, but it also saves fuel and reduces emissions.

But keeping hydrocarbons in the ground, especially oil and gas, is virtually impossible because of the degree the products derived from them are imbedded in our lives and economies and, importantly, how they improve them. Many of us in the energy business were treated to a CEO of an oilfield service company educating the CEO of a clothing company about the importance of fossil fuels. Adam Anderson, CEO of Innovex Downhole Solutions, wrote to Steve Rendle, the head of VF last fall after North Face turned down his request to purchase about 400 jackets with his company’s logo on them as Christmas gifts for employees. North Face turned the order down, according to Anderson, because “They said we don’t meet their brand criteria.” He told the media that North Face did not want to be associated with certain industries and mentioned “alcohol, tobacco and porn.”

The four-page letter Anderson wrote to Rendle received wide publicity as it succinctly laid out the case for hydrocarbons and the good things they have delivered for humanity. Moreover, Anderson was cheered for standing up for the petroleum industry against the “counterproductive virtue signaling” of North Face. The irony that North Face’s products are all made from petroleum products, and the activities and lifestyle promoted by the company depends currently on fossil fuels, seemed to be lost on its management.

As we have seen and heard more about why we need to do away with fossil fuels in recent weeks, we are responding to questions from readers to show the importance of petroleum in the every-day lives of humans. The Department of Energy’s Fossil Fuel division published a one-page graphic that contained a list of products coming from petroleum. We have captured their list below:

Adhesive, Air mattresses, Ammonia, Antifreeze, Antihistamines, Antiseptics, Artificial limbs, Artificial turf, Asphalt, Aspirin, Awnings, Backpacks, Balloons, Ballpoint pens, Bandages, Beach umbrellas, Boats, Cameras, Candies and gum, Candles, Car battery cases, Car enamel, Cassettes, Caulking, CDs/computer disks, Cell phones, Clothes, Clothesline, Clothing, Coffee makers, Cold cream, Combs, Computer keyboards, Computer monitors, Cortisone, Crayons, Credit cards, Curtains, Dashboards, Denture adhesives, Dentures, Deodorant, Detergent, Dice, Dishwashing liquid, Dog collars, Drinking cups, Dyes, Electric blankets, Electrical tape, Enamel, Epoxy paint, Eyeglasses, Fan belts, Faucet washers, Fertilizers, Fishing boots, Fishing lures, Floor wax, Food preservatives, Footballs, Fuel tanks, Glue, Glycerin, Golf bags, Golf balls, Guitar strings, Hair coloring, Hair curlers, Hand lotion, Hearing aids, Heart valves, House paint, Hula hoops, Ice buckets, Ice chests, Ice cube trays, Ink, Insect repellent, Insecticides, Insulation, iPad/iPhone, Kayaks, Laptops, Life jackets, Light-weight aircraft, Lipstick, Loudspeakers, Lubricants, Luggage, Model cars, Mops, Motorcycle helmets, Movie film, Nail polish, Noise insulation, Nylon rope, Oil filters, Packaging, Paint brushes, Paint roller, Pajamas, Panty hose, Parachutes, Perfumes, Permanent press, Petroleum jelly, Pharmaceuticals, Pillow filling, Plastic toys, Plastics, Plywood adhesive, Propane, Purses, Putty, Refrigerants, Refrigerator linings, Roller skate wheels, Roofing, Rubber cement, Rubbing alcohol, Safety glasses, Shampoo, Shaving cream, Shoe polish, Shoes/sandals, Shower curtains, Skateboards, Skis, Soap dishes, Soft contact lenses, Solar panels, Solvents, Spacesuits, Sports car bodies, Sunglasses, Surf boards, Swimming pools, Synthetic rubber, Telephones, Tennis rackets, Tents, Tires, Tool boxes, Tool racks, Toothbrushes, Toothpaste, Transparent tape, Trash bags, Truck and automobile parts, Tubing, TV cabinets, Umbrellas, Unbreakable dishes, Upholstery, Vaporizers, Vinyl flooring, Vitamin capsules, Water pipes, Wind turbine blades, Yarn

Think not only of what goes into these products but also the energy necessary to make them. Are there alternatives? In some cases, yes, but often they come with environmental costs that may outweigh the CO2.

In doing our research, we also came across a listing of petroleum-derived items prepared by Steve Pryor, a consultant in energy asset optimization and energy trade and risk management. The list was prepared in 2016 and titled “A Partial list of the over 6,000 products made from one barrel of oil (after creating 19 gallons of gasoline).” Initially in his write-up, Pryor discussed the more readily identifiable items coming from the 42-gallon barrel of crude oil, primarily gasoline (19.4 gallons), but also jet fuel and heating oil. He also pointed out that “all plastic is made from petroleum and plastic is used almost everywhere: in cars, houses, toys, computers, and clothing. Asphalt used in road construction is a petroleum product, as is the synthetic rubber in the tires. Paraffin wax comes from petroleum, as do fertilizer, pesticides, herbicides, detergents, phonograph records, photographic film, furniture, packaging materials, surfboards, paints, and artificial fibers used in clothing, upholstery, and carpet backing.” While his listing of products coming from petroleum is encompassing, he also included another long list of specific items made from petroleum. What we found, however, were numerous repetitions in the listing, so we are not sure about the 6,000 total items he alluded to, although his list came nowhere near that total. We have gone through his list (below) and hopefully eliminated all the duplications.

Products made from petroleum include: Solvents, Diesel, Motor Oil, Bearing Grease, Ink, Floor Wax, Ballpoint Pens, Football Cleats, Upholstery, Sweaters, Boats, Insecticides, Bicycle Tires, Sports Car Bodies, Nail Polish, Fishing lures, Dresses, Tires, Golf Bags, Perfumes, Cassettes, Dishwashers, Tool Boxes, Shoe Polish, Motorcycle Helmets, Caulking, Petroleum Jelly, Transparent Tape, CD Player, Faucet Washers, Antiseptics, Clothesline, Curtains, Food Preservatives, Basketballs, Soap, Vitamin Capsules, Antihistamines, Purses, Shoes, Dashboards, Cortisone, Deodorant, Footballs, Putty, Dyes, Panty Hose, Refrigerant, Percolators, Life Jackets, Rubbing Alcohol, Linings, Skis, TV Cabinets, Shag Rugs, Electrician’s Tape, Tool Racks, Car Battery Cases, Epoxy Paint, Mops, Slacks, Insect Repellent, Oil Filters, Umbrellas, Yarn, Fertilizers, Hair Coloring, Toilet Seats, Fishing Rods, Lipstick, Denture Adhesive, Linoleum, Ice Cube Trays, Synthetic Rubber, Speakers, Plastic Wood, Electric Blankets, Glycerin, Tennis Rackets, Rubber Cement, Fishing Boots, Dice, Nylon Rope, Candles, Trash Bags, House Paint, Water Pipes, Hand Lotion, Roller Skates, Surf Boards, Shampoo, Wheels, Paint Rollers, Shower Curtains, Guitar Strings, Luggage, Aspirin, Safety Glasses, Antifreeze, Football Helmets, Awnings, Eyeglasses, Clothes, Toothbrushes, Ice Chests, Footballs, Combs, CD’s, Paint Brushes, Detergents, Vaporizers, Balloons, Sun Glasses, Tents, Heart Valves, Crayons, Parachutes, Telephones, Enamel, Pillows, Dishes, Cameras, Anesthetics, Artificial Turf, Artificial limbs, Bandages, Dentures, Model Cars, Folding Doors, Hair Curlers, Cold cream, Movie film, Soft Contact lenses, Drinking Cups, Fan Belts, Car Enamel, Shaving Cream, Ammonia, Refrigerators, Golf Balls, Toothpaste, Gasoline, Dishwashing liquids, Toys, Unbreakable dishes, Dolls, Car sound insulation, Refrigerator linings, Glue, Soap dishes, Skis, Permanent press clothes, Hand lotion, Disposable diapers, Salad bowls, Electric blankets, Awnings, Ammonia, Dresses, Safety glass, Pajamas, VCR tapes, Movie film, Loudspeakers, Credit cards, Roofing shingles, Shower curtains, Garden hose, Plywood adhesive, Milk jugs, Beach umbrellas, Sun glasses, Luggage, Wire insulation, Folding doors, Shower doors, Cortisone, Carpeting, Artificial turf, LP records, Hearing aids, Wading pools.

As you read the list, it becomes clearer how much our daily lives depend on petroleum. To put that involvement into perspective, Americans use, directly and indirectly, 2.8 gallons of crude oil a day, based on the daily average taken from the 4-week average of the amount of oil and product supplied to the nation for the week ending February 18, 2022, and 269 cubic feet of natural gas, based on the daily average consumption for November 2021, the latest monthly data available. Based on $92 per barrel and $4.50 per thousand cubic feet, prices at the time we did this calculation, the daily cost of petroleum used by Americans was $7.37 ($6.13 + $1.24), or about the price of a quarter pounder at McDonalds.

It is a sobering realization that transitioning the manufacture of these products to non-petroleum-based materials will be a long process, if even possible. While there may be alternatives available, in some cases there are no options regardless of the cost. The lists above drive home the difficult challenge of the energy transition, and why petroleum will play a role in our energy mix for decades to come.

Thoughts On Random Energy Topics

Europe’s Infatuation With Heat Pumps Has A Long Way To Go

One of the tenets of Europe’s clean energy transition is to get homeowners to replace their gas furnaces with heat pumps and biomass stoves, thereby reducing fossil fuel use. Heat pumps are designed to run on electricity generated by wind and solar power. A recent commentary from a newsletter that focuses on clean energy technology pointed out that in 2021, heat pump sales in Europe were growing rapidly. In France, they grew by 52% to 267,000 installations. That is a healthy growth rate. However, the figure represents slightly less than 1% of French homes. Poland’s heat pump market experienced a strong 2021 with installations increasing by 66% to about 92,000 units. But this represents a smaller market share than seen in France. At those growth rates, France and Poland may have many years of comparable installation rates before materially impacting their respective fossil fuel consumption. We assume neither country is mandating a transition to heat pumps, as in the U.K., therefore, these low market penetration rates are likely a function of the economics of their purchase and use.

The more interesting data the newsletter contained dealt with France’s biomass stoves – those that burn wood pellets. Installation of 34,000 stoves occurred in 2021, expanding the installed base of biomass stoves by more than 100%. Suddenly, there is concern about the long-term sustainability of the European supply of wood pellets. The 2021 French stoves will use approximately 4% of the country’s total softwood production. That suggests in a few years France could experience what befell New England in the 1700s after the colonists consumed all the mature forests of the region, we needed a second generation of forests to grow to continue the wood-burning. The emergence of coal at this point saved the new trees from being cut down.

A Blow To Renewable Power In Germany Confirms Market Disruption

A brief news item said that German wind turbine producer Nordex has shut down its rotor blade manufacturing plant in Rostock. Some 600 jobs were lost. Executives at Nordex blamed the government’s switch from a negotiated subsidy program to an auction system for undercutting the economics of the turbines. In other words, when auctions are used to promote renewable energy, the economics are dictated by the lowest cost of bidders. We never know exactly what influences the bidding strategies of developers as they are fighting to win projects. It is possible that financially stronger developers are using low price bids for the electricity to drive competitors from the market, while hoping that as their projects expand, they can negotiate better pricing for wind turbines that help them improve project economics marginally. We do not know if this is happening or not. We also do not know how many developers are abandoning wind projects because of the rising cost of turbines that are destroying their economics. But this is the first tangible evidence of wind projects not going forward – market disruption – as suggested would happen by the CEOs of wind turbine equipment manufacturers when discussing their cost problems. They acknowledged that raising the price of wind turbines to solve their financial problems would saccade through the industry causing pricing problems for their customers. That obviously is happening.

1970s Energy Crisis Playbook Is Being Resurrected

We have seen multiple reports that European Union officials are telling member countries to implement windfall profits taxes on the energy companies who are benefitting from high oil, gas, coal, and electricity prices. Moreover, they are telling the governments to use the money to invest in clean energy projects. As Reuters wrote in a story last week about the International Energy Agency’s (IEA) 10-point plan on how Europe can reduce its reliance on Russian energy sources:

The IEA outlined short-term measures such as redirecting windfall profits made by energy firms, secured from high gas prices, to support customers facing higher bills.

The European Commission is expected to propose that member states tax windfall profits of energy companies to support investment in renewables and compensate customers.

In the 1970s, when the U.S. government created a byzantine energy tax and control system to deal with the explosion in oil prices, all market price signals for supply and demand were distorted, creating other problems and longer-lasting issues.

Consumers were forced to deal with odd and even day rules for buying gasoline. Hours-long gasoline station lines were created by the bureaucracy allocating fuel supplies to states based on past population and consumption data, all of which was out of date, especially for rapidly growing states. Speed limits on highways were reduced to 55 miles per hour to save fuel, and people were urged to lower their thermostats to safe on home heating.

Oil companies wrestled with the definition of each barrel of oil they produced. Was it an “old,” a “new,” or a “new-new” barrel? Each category was allowed to be sold at a different (progressively higher) price. Heaven help you if you got the classification wrong! We shudder to think we might have to revisit our personal archives to relearn the language and nuances of 1970s energy pricing and regulations to help our readers navigate the next several years.

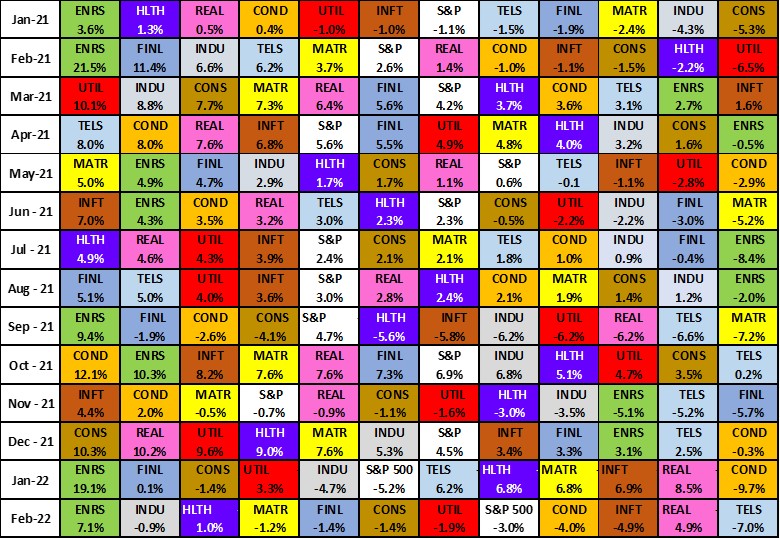

The Energy Super-Cycle Is Rewarding Investors In The Sector

There is increasing evidence that investors, especially institutional investors, are shifting funds away from high tech, telecommunications, and other highly valued stocks and into commodity and basic industry stocks, especially in the energy sector (green). We have updated our favorite S&P 500 sector chart showing the monthly performance of the eleven sectors and the entire S&P 500 index since January 2021.

Exhibit 13. The Monthly Performance Of S&P 500 Index Industry Sectors

Source: S&P, PPHB

As the chart shows, it was either feast or famine for energy during this 14-month span. That is not surprising when tracking monthly performance because stock groups often suffer significant profit-taking following months of very strong positive performance. During the 14 months, energy was either the best (five times) or second-best (three times) performing sector for a total of eight months. In the other six months, energy was either the worst (three times), second worst (once) or third worst (twice) performing sector. There was no middling performance for energy. Love it or hate it seemed to be investor sentiment. Do not expect much to change this year, as energy prices will likely remain high given geopolitical developments and the tight global supply/demand balance for crude oil and natural gas. That assumes world economies do not crash during 2022. Add to those fundamental drivers the point we have made in the past that professional investors can only underperform for a limited time-period before they are pressured to buy the best performing stocks. All the financial data and anecdotal evidence confirms that these investors are buying energy stocks now.

Offshore Wind Is Taking Its Lumps

Three quick news items about the offshore wind business that emerged in the last few days. First, a study by Common Weal of the Scottish offshore wind industry development and recent lease sale takes the government to task for not establishing its own energy company to conduct the sale and buy the power, which it says would have put billions of pounds into the government’s coffers. (We will have more on this once we study the report.) What caught our eye was the statement that 12 years ago the government claimed there would be 28,000 workers in the offshore wind business by 2020. Industry data for 2019 showed just 1,400. A warning about believing the economic and employment benefit claims from wind farm promoters.

The second item was the announcement that New Jersey is delaying solicitation of interests in its third offshore wind lease sale from September 2022 to January 2023. Reasons offered for the delay included giving the winners in the New York Bight offshore wind lease sale time to assess their plans and how those might fit with the New Jersey sale, but also, because the government received 80 proposals for constructing an offshore power transmission line that needed more time for evaluation. It sounds to us like there must be some highly profitable aspect to this cable project to generate such a high level of interest. We are not sure why that is, but we will be investigating. Another land-grabbing opportunity?

The third development is the battle in Massachusetts over new legislation governing the future of the state’s offshore wind business. The statehouse reporter for newburyportnews.com described the legislation.

The legislation, which was approved by a vote of 144 to 12, calls for accelerating the development of offshore wind by changing how the state procures the energy, creating tax credits for offshore wind companies and setting environmental and fishing industry requirements for offshore wind projects, among other changes.

The proponents of the new legislation claim it would position Massachusetts to become the “Saudi Arabia of wind.” At issue is the removal of the cap on electricity prices, which is said would alter and complicate the bidding process for new offshore wind farms. The legislation’s sponsor claims that with development costs falling, electricity prices will not rise under this move. Moreover, he says that regulators could reject expensive power price deals.

Others push back, especially ratepayers who see higher electricity prices on the horizon, just as they are experiencing sharply rising power costs this winter. Maybe they are reading the stories about the financial problems of wind turbine manufacturers and the need for them to raise their prices. The ratepayers are also questioning the proposed surcharge on natural gas bills that would boost their annual costs by about $10 a year. The surcharge is to help fund the cost of expanding renewable energies. According to the latest Massachusetts data, 52% of homes in the state heat with gas, 26% use oil or kerosene, 16% use electricity, and the balance use various other fuels or have no heat. Thus, over half the state’s residents would be impacted by the surcharge. If renewable energies are so cheap, why the need for a surcharge on half the state’s population to fund new renewable energy projects?

The fishing industry is organizing opposition to the bill and is mobilizing its legislative friends who are offering amendments to protect the fishing interests. Given what is going on in the offshore wind business and in energy markets today, coupled with inflationary and interest rate pressures, count us skeptical of the benefits and leery of future costs. Politicians are always looking backwards as they design legislation and rules for the future.

Contact PPHB:

1885 St. James Place, Suite 900

Houston, Texas 77056

Main Tel: (713) 621-8100

Main Fax: (713) 621-8166

www.pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 150 transactions exceeding $10 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.