Energy Musings contains articles and analyses dealing with important issues and developments within the energy industry, including historical perspective, with potentially significant implications for executives planning their companies’ future. While published every two weeks, events and travel may alter that schedule. I welcome your comments and observations. Allen Brooks

November 29, 2022

Energy Market Outlook Seen By Investors And Analysts

Observations from RBC energy investor survey and Fed Bank energy conference provide a set of unconventional views of energy markets and their future along with how energy stocks may trade. READ MORE

Inflation And Interest Rates Continue To Roil Energy Markets

Investors think inflation has peaked but the real world seems to just begin seeing its impact and higher interest rates are proving a problem. Gavekal Research shows a different perspective. READ MORE

New England’s Winter May Not Be Fun As It Will Be Costly

Heating oil and electricity prices have soared with supply shortage fears, so weather will determine how costly winter is. Forecasts suggest a normal winter with periods of severe cold. READ MORE

Europe’s Energy Wildcards Less Effective Than Anticipated

Russia oil ban and Europe oil and gas price caps may be less effective than originally thought. Politics have created regulations that hold potential for market chaos and underground options. READ MORE

Random Energy Topics And Our Thoughts

- Can You Reach Net Zero By 2050?

- New England Offshore Wind Market Declining Into Chaos

- COP27 – A Cop Out?

Energy Market Outlook Seen By Investors And Analysts

The seventh joint energy conference of the Dallas and Kansas City Federal Reserve Banks was recently held in Houston and an array of energy industry analysts, consultants, and executives presented and discussed a wide range of issues impacting the industry’s outlook. There were numerous observations from presenters that deviated from conventional views telegraphed by the stock market or in statements and policies about energy markets from the Biden administration. Many of these observations are related to issues impacting climate change and the push for renewables over fossil fuels.

The following are some observations that we found interesting. Ellen Wald of Transversal Consulting commented on Russia’s oil export problem when the European Union’s (EU) ban on oil purchases goes into effect on December 5th and later its ban on purchases of refined petroleum products starts. She believes Russia will be able to continue exporting oil, but not as much to China as some analysts expect. In her view, China will not take more than three million barrels per day to not become dependent on Russian supplies. This means Russia will be seeking a home for a meaningful amount of its current oil production. The EU ban, with its price cap on Russia’s oil price, is the wildcard in everyone’s forecast for oil prices as we end 2022.

Brenda Shaffer of the Naval Postgraduate School gave a fascinating presentation on natural gas. She pointed out that natural gas was mentioned 56 times in the government’s most recent national defense strategy report, but always it was mentioned in conjunction with renewables and climate change. In her view, these comments were not reflective of the current energy situation.

Shaffer pointed out how natural gas during the 1990s and 2000s was favored for our energy mix because of its economic and environmental benefits. Today, natural gas is considered in conjunction with renewables, but these two fuels are positioned as a binary choice. One is good, the other is bad, and you can’t have both. She disagrees and believes they go together as gas supports renewables in the power generation market.

She also focused on forces that are impacting the energy market. For example, natural gas requires active involvement by the government because of the need for approvals for pipelines and export terminals. In contrast, most of our oil and coal business goes on under the radar, so it is less impacted by government actions.

She suggested that we are not in an energy transition. That is because we are a fossil fuel-oriented economy, and actions to force a transition will create future problems. She pointed to questions such as: Will the EU allow long-term gas contracts? Will the U.S. allow public financing of fossil fuel projects? She pointed to the history of the United States as having financed the development of many international oil and gas infrastructure projects that have made the global energy system more efficient and improved living standards. Now, China is filling that role, which raises questions about what it will gain in the future from these investments. She noted how in both Europe and Asia, governments are working to nationalize utilities and energy, giving bureaucrats and politicians much greater power in the energy market. Of course, these are decision-makers with little practical knowledge of the workings of the industries they are regulating. But the most shocking comment was her answer to the question: How did we get into this energy crisis? Her answer is stockholder capitalism under the guise of the ESG (environmental, social, and governmental) movement. In her view, natural gas remains the cheapest way to improve our environment by reducing pollution.

The final speaker on the panel addressing “Shifts in Energy Geopolitics” was Morgan Bazilian, who heads the Payne Institute for Public Policy at the Colorado School of Mines. He began by pointing out that he authored a book in 2008 where he made the point of Europe’s need for energy diversification to protect against becoming too dependent on Russian natural gas. Guess what?

He based his presentation on the reality that all energy policies are based on political priorities. So, France blocked long-term U.S. liquefied natural gas (LNG) deals because they considered the fuel “too dirty.” Remember that correcting this policy was President Donald Trump’s first order of business when he attended his first G7 meeting at which he was pictured being harassed by Germany’s Angela Merkle and other European leaders over his view about Europe’s wrongheaded energy strategy.

Bazilian said that there was “probably not one country that has climate change as a priority” that would be attending the upcoming COP27 climate change conference. In his view, “energy security is the priority.” Those observations seem to have been borne out at COP27’s conclusion.

In his view, the energy transition is about developing economies. He believes that a zero-carbon world does not do away with zero-sum games. He also believes that the pace of change matters a great deal, but most importantly, we should shift our attention away from climate goals and toward pathways to get there. In that regard, his organization tracks and reports on critical minerals needed in the clean energy transition. The list of these minerals has expanded from 35 to 50 over just the past 18 months. The major problem in understanding the markets for these minerals is that they are “tiny, opaque, dirty, and controlled by nasty governments.” In his view, the net zero utopias of climate change activists will not happen.

Bazilian’s view on net zero emissions was interesting when later in the program, Ashish Sethia of BloombergNEF essentially agreed. First Sethia discussed the global renewables outlook. While acknowledging that renewable energy costs are going up, he believes it is all due to supply chain issues and that when they are resolved, costs will begin to go down again. Unfortunately, he never clarified what supply chain issues he was referencing and possibly how long it would take to be resolved. He reiterated his firm’s research that shows we need to invest $1.7 trillion a year up to 2030 to keep the world on track for net zero. He also said that without Carbon Capture and Underground Storage, to get to net zero emissions we will need 20-30 times the amount of clean energy fuels currently envisioned. His most telling comment came in response to a question about the impact of rising interest rates, which he sees as restricting investment in energy supplies and ensuring that net zero will not happen.

There were many other presentations with interesting data and observations. But on the day of the conference, the consumer price index (CPI) data was released showing less inflation than expected, and oil prices fell by just over 3%. This was just one of many days recently when we have seen huge swings in oil prices, usually driven by changes in expectations for future demand or supply. The November 10th oil price drop on better inflation news was strange as the economic news should have been perceived to be positive for future economic activity and oil demand. Of course, speaking at the Fed energy conference was Ester George, president of the Kansas City Fed and a member of the Federal Open Market Committee that establishes short-term interest rates. Her talk was hawkish about the need to raise interest rates more than expected and keep them high for longer than people anticipate for corralling inflation.

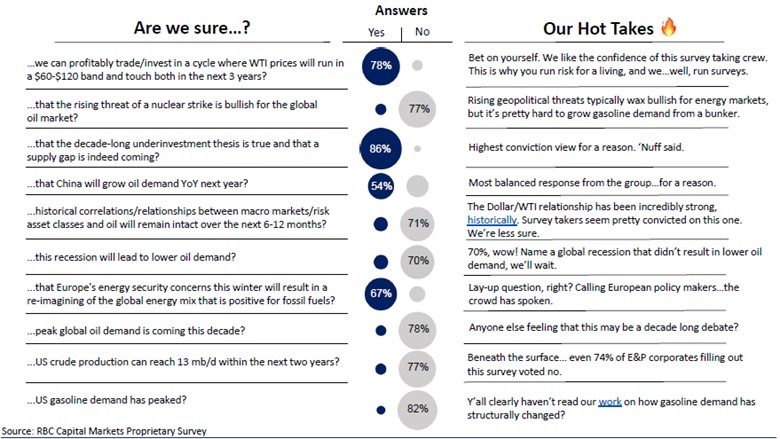

Trying to understand oil price gyrations has become challenging. Fortunately, Michael Tran, the Commodity and Digital Intelligence Strategist for RBC Capital Markets, LLC, published the results of his firm’s survey of various groups of investors and their attitudes toward oil investing. The groups of investors fell into five categories: Macro Investors; E&P Corporates; Generalist investors; Energy Specialist Investors; and Commodity Hedge Funds & Trading Houses.

Each category of investors has different objectives, as well as different approaches to investing in energy stocks. The bullet points from the survey summary of all the views collected, and sometimes Tran’s observations were both interesting and telling when trying to understand oil price and energy stock volatility. One of the most surprising facts to emerge from the survey was that generalist equity investors made up 38% of total responses. Tran and his team viewed this high percentage as a sign of high engagement by investors. But does it signal that the rush to invest in energy securities is at risk of peaking? Here are the three key bullet points from the survey:

- 67%…of you expect that Europe’s energy security concerns this winter will result in a reimaging of the global energy mix that is net positive for fossil fuels.

- 77%…of respondents are skeptical about US crude production reaching 13 mb/d over the next two years.

- 82% The percentage of respondents refused to believe that US gasoline demand has peaked. We’ll take the other side.

An interesting part of the survey was RBC’s asking: “Are we sure…?” Tran commented that many responders thought they were being led to an answer because of the question leading off the survey. Rather, Tran believes that the binary response prevents responders from hiding behind “ifs,” “ands,” “buts,” or “maybes.” Therefore, the response provides a view into the mainstream, long assumed to be consensus ideas that get resounding yes answers. These topics included ones that RBC’s team is not sure of, so they were hoping to generate deeper thought about them. It seems to have worked. All the topics and responses are shown below.

Exhibit 1. Investor Views Versus Conventional Thinking About Oil

Source: RBC Capital

We already highlighted several of the conclusions presented in the above table. What was intriguing was the 86% Yes response to the theme that extended underinvestment in energy will create a supply gap that will make this an extended cycle for oil prices. What is not surprising about this response is that there is and has been little true frontier oil and gas exploration seeking new basins or testing for new horizons in underexplored basins. Another way of expressing this supply issue is questioning where the next Guyana or Permian Basin is, as they may be the key to extending the oil age.

While the Dallas and Kansas City Federal Reserve Banks’ energy conference was heavily weighted towards oil and natural gas, renewables did receive reasonable attention. However, those renewables presenters acknowledged that their futures would take longer and cost more than is popularly thought. And with the RBC survey, we see the views of energy that are shaping investors’ thoughts. If there is wisdom in crowds, both the survey respondents and the RBC commodities group may be in for future surprises. What we conclude from the conference and the survey is that energy is well-placed to be an important driver in our economy for years to come, albeit with significant volatility.

Inflation And Interest Rates Continue To Roil Energy Markets

On November 10th, the Dow Jones Industrial Average surged 1,198 points marking the largest one-day increase in the index since 2020. The surge was driven by the release of October’s Consumer Price Index (CPI) showing prices only rose 0.4% or 0.3% excluding food and energy – the core inflation rate. These increases were below investor and analyst expectations. The CPI annual rate fell to 7.7%, the lowest since January. Core inflation declined to a 6.3% annual rate versus views it would stay at a 40-year high of 6.6%. The stock market’s response to the inflation data marked a swift shift in investor sentiment about inflation and its future trajectory. The path of inflation is open to debate as some analysts and economists expect it to fall sharply while others expect a much slower rate of decline.

A major contributor to the CPI decline, which was later supported by a decline in producer prices, was falling energy prices. But the bigger question is where the inflation rate decline might settle. Those economists projecting a rapid collapse in inflation expect it to settle back in the vicinity of the Federal Reserve Board’s target of a 2% or so average annual rate of increase. Other economists believe it will take years, not months, for the CPI rate to reach the Fed’s target zone. Still, other economists expect inflation will land at a lower rate but be sustained at a higher level than experienced recently for years to come.

Where inflation ultimately settles will be important for the economy, but its greater power will be on the future level of interest rates. Central banks have been raising their base lending rates to help slow their economies and choke off high inflation by reducing demand. The impact of this strategy has been uneven across the globe, largely depending on what energy inflation rates are in the various countries. European economies are suffering under soaring energy costs that drive overall inflation rates up sharply and erode demand rapidly, driving economies toward recessions.

Higher sustained inflation and interest rates will take a toll on economies and present challenges for businesses and policymakers. One industry exhibiting problems in coping with these economic pressures has been wind energy. Manufacturers of wind turbines have been slammed by exploding prices for raw materials needed for their products that have forced companies to raise prices that cut market growth. Solving this problem is forcing significant restructuring steps by the manufacturers, and ultimately the wind farm developers.

Comments from Marc Becker, CEO of Siemens Gamesa’s offshore wind business unit, at the recent Recharge Global Offshore Wind Summit highlight the new economic realities that are impacting his industry and company. He commented on the disruption of supply chains from Covid, inflation, and the Ukraine war. “I think we have to recognize this change – and I think that’s something that has not completely made its way through. The impact is that costs are going up – and they will continue to go up,” he said. Bad news for wind turbine buyers.

As an example of what these relentlessly rising costs are doing to wind turbine manufacturers, consider the observation of Henrik Andersen, chief executive officer of Vesta, the world’s largest turbine maker. He recently told The New York Times, “Every time we sell a turbine, we lose 8 percent.”

Recharge reporters writing about Becker’s comments point to questions of project viability based on economic analysis done before what he called “a different world” of spiraling costs emerged. Becker went on to say that we “need to see different prices or [the] energy transition will be delayed.” He went on to note “It’s not an easy topic because it comes with a new ton of problems [but] this new reality has to be appraised and taken into account, because… otherwise there is no sustainable industry.” His final plea to fellow wind energy executives was “The sooner we appraise the topic and work on it the better. We can overcome this challenge, but we need to recognize it.”

The different world of spiraling costs has already inflicted damage on Becker’s company as well as others. The New York Times recently reported, “This month, Siemens Gamesa Renewable Energy, a Madrid-based company that is the premier maker of offshore wind turbines, reported an annual loss of 940 million euros ($965 million). The company has announced a cost-cutting program that is likely to lead to 2,900 job losses, or nearly 11 percent of its work force.” This is not the only company in the renewables industry to recognize and take action to adjust to this different world.

Becker’s plea for industry executives to recognize the new realities and adjust accordingly would also appear to be behind Avangrid’s move to seek price adjustments for their Massachusetts power purchase agreements for their offshore wind farms. (We write about this elsewhere.) Other offshore wind project developers have also commented on the need to revisit their project’s economics.

Recognition of the new reality was also embraced by General Electric Chairman and CEO Larry Culp who noted on its recent third-quarter earnings call with investors that it would be restructuring the operations of its renewable energy division, soon to be spun off as an independent company. In the third quarter, that division’s revenues fell by 15% as developers delayed placing orders for new turbines as the expiration of the current U.S. production credit had them waiting for the new subsidies available under the Inflation Reduction Act that will commence next year. The division also needed to add $500 million to warranty reserves reflecting recent quality issues, which helped drive the nearly $1 billion loss in the quarter, a sixfold increase from a year ago. GE expects its renewable business to post a $2 billion pre-tax loss for all of 2022.

The GE renewables business unit will undergo a massive restructuring that will cost roughly $600 million but, if successful, save the company about $500 million in costs annually. It includes cutting one of out every five onshore wind jobs and “more broadly delayering” elsewhere in the renewables group. This restructuring, aimed at cutting jobs as well as improving internal processes, matches changes underway at every other wind equipment manufacturer. Everyone is downsizing employment, defeating the claim that the wind industry will be a job creator.

What happens if inflation has not peaked? Could this derail the stock market’s euphoria? More importantly, will it guarantee a recession in the new year to slow inflation and sustained higher interest rates? This latter change goes to the issue of the need to adjust pricing that Becker of Siemens Gamesa was illuminating for his audience at the Recharge conference.

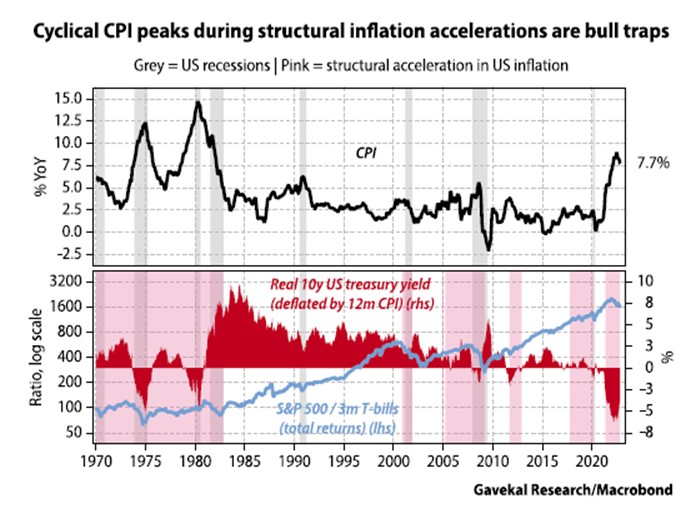

A recent analysis by Charles Gave of Gavekal Research addressed the question of the peaking in inflation. He concluded it has not. He believes the stock market reaction to the CPI data was premature. His conclusion is based on two observations from the following chart.

He points out “The upper pane shows that over the last 50 years, every significant peak in the US rate of inflation has occurred during a recession or just after. So, if inflation peaked in October 2022, then there are only two possibilities:

1) The US economy is already in a recession, which will be confirmed retrospectively, as usual. This is possible, but not likely.

2) This time is different. For structural reasons, this is highly unlikely.”

Exhibit 2. Inflation, Recessions, Yields, And Stock Market Have Tight Relationships

Source: Gavekal Research

Gave goes on to write:

Now look at the lower pane of the chart. The areas shaded pink represent periods when US inflation was undergoing structural acceleration, defined as when the two-year trend in inflation was steeper than the 15-year trend. The red bars show the real yield on 10-year US treasuries. And the blue line is the ratio between total returns on the S&P 500 and on three-month treasury bills, as a proxy for cash.

Here we see something crucial. In 1970, 1974, 1980 and 2008 we saw cyclical peaks in inflation during periods when inflation was accelerating structurally. Each was a massive bull trap, as almost every time the S&P 500 underperformed cash.

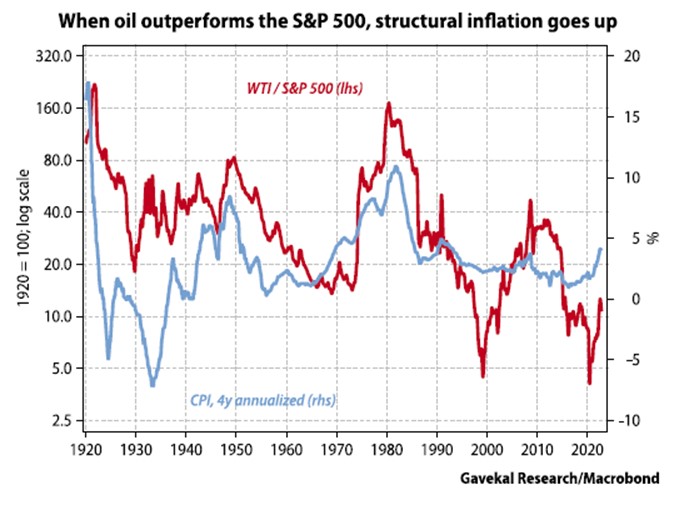

In Gave’s opinion, bull markets for stocks occur when energy is cheap and getting cheaper. Bear markets happen when energy is expensive and becoming more expensive. He points out that “today energy is getting more expensive.” To prove that point, he points out that “Since mid-2020, the price of oil has been outperforming the S&P 500,” something he expects will continue: “Historically, U.S. inflation has almost never peaked when the price of energy has been rising faster than the S&P 500.” Gave illustrates that point in the following chart showing the ratio of oil prices (WTI) to the S&P 500 index compared against the 4-year annualized CPI index, a measure of long-term price trends.

Exhibit 3. Oil And Stock Market Signal Inflation Will Be Long Lasting

Source: Gavekal Research

Gave’s research and an earlier analysis he prepared on oil prices that he concludes shows a 30-year energy cycle, fits with the “super-cycle” for oil that Goldman Sachs’ commodity expert Jeff Currie has been highlighting. Rising energy costs will help keep inflation higher than the Federal Reserve’s 2% annual target. It will also contribute to higher interest rates that must be sustained to try to keep inflation under control. These forces will be joined by the relentless push for renewable energy, which is proving to be more expensive than advertised, which will also be a long-term driver of higher inflation.

We have entered a new normal for the economy, although many still do not believe it. This new normal will be marked by higher inflation and higher interest rates, both of which will upset economic and business plans currently in place. As Siemens Gamesa’s Becker urged his audience: “The sooner we appraise the topic and work on it the better.” That is an important message for business executives across the world, including energy executives who are just beginning to experience problems with their supply chains, labor availability, and overall cost issues.

New England’s Winter May Not Be Fun As It Will Be Costly

Although New England avoided the lake-effect snowmageddon that hit the Buffalo area recently, it is holding its collective breath for the upcoming winter. The warnings about possible power blackouts due to energy shortages and soaring demand this winter have already been delivered by ISO-NE, the operator of the region’s electric grid. That is because of the region’s dependency on natural gas. New England is also low on distillate inventories heading into winter, which is concerning because of the region’s high dependency on oil for heating. During the 2020-2021 winter, according to the Energy Information Administration, of the 5.3 million U.S. homes heated with oil, nearly four million, or 85% were in the Northeast. Additionally, when the region’s electricity system is short of natural gas, its power plants burn oil and sometimes coal.

Concern about the upcoming winter power and heating situation prompted Joseph R. Nolan, Jr., the president and chief executive officer of Eversource Energy, one of the region’s major electric utilities, to write to President Joe Biden asking for him to declare an emergency that would allow extraordinary steps to be taken such as a waiver for the Jones Act, an emergency order under the Natural Gas Policy Act, and an emergency authorization under the Defense Production Act. These actions would enable the government and its agencies to overrule market and contract agreements to ensure an adequate supply of natural gas and other fuels to heat and power the region.

Exhibit 4. Are People Ready For Winter And Sky-High Utility Bills?

Source: FT.com

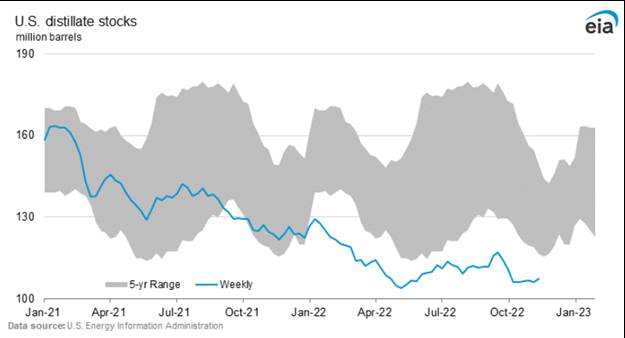

We know that distillate inventories nationwide are low, but this is a particularly dangerous situation in New England because of its high dependence on that fuel for home heating. Nationally, the concern over the low distillate inventory is because of its potential impact on the transportation sector – trucks, trains, and barges – which is the lifeblood of the economy. Nearly everything we purchase, and use is delivered by trucks that use diesel. The following chart shows the past two years’ level of U.S. distillate inventory compared to the range for the past five years. Current inventory levels are around 26 days of consumption, which has led some media and analysts to claim the nation is close to running out of distillate. That would only happen if our national refining industry were to be shut down. However, we are going to be challenged to manage our thin supplies.

Exhibit 5. The Woeful State Of The Nation’s Distillate Inventory

Source: EIA

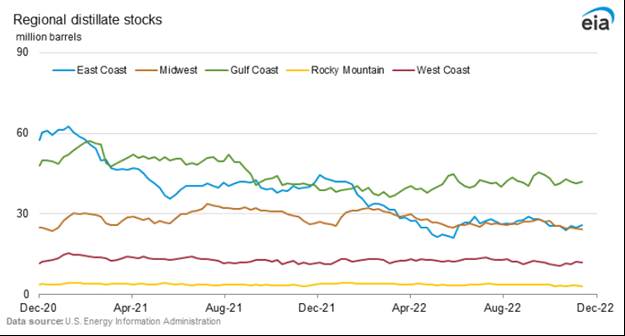

On a regional basis, New England is concerned because of the dramatic decline in distillate inventories over the past two years. The following chart shows each U.S. geographic region’s distillate inventory for 2021 and 2022 so far. From roughly 60 million barrels of inventory in December 2020, the New England region, as of November 11, had only 26 million barrels, down from 40 million barrels a year ago. The only good news is that reports indicate there is a flotilla of 11 ships heading to the U.S. from Europe with 3.6 million barrels of supply.

Exhibit 6. Distillate Inventories For 2021-2022 By Region Of The Country

Source: EIA

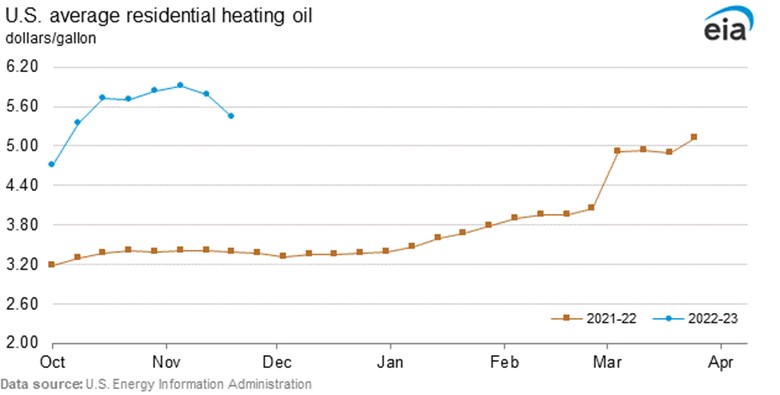

The result of the low distillate inventory is that prices have soared. As the EIA chart below shows, the most recent heating oil price at $5.43 a gallon is $2.05 higher than a year ago. Distillate prices began climbing in the later weeks of last winter and then jumped up this October as consumers realized the possibility of a supply shortage this winter. But with continuing declines in distillate inventories, the price jumped this fall and rose further, nearly topping the $6 a gallon level, but a wave of warm weather has caused prices to dip.

Exhibit 7. Residential Heating Oil Prices Are Near $6 A Gallon

Source: EIA

For New England heating customers, if they were paying $300 a month last year, this year’s monthly bills will be more than $200 higher. For a five-month heating season, the higher fuel oil price will cost an additional $1,000 or more this winter. For many residents, paying these higher monthly heating bills will be a challenge.

The natural gas situation is equally challenging for New Englanders because the ability to add more supply depends on new or expanded pipeline capacity – not happening – or through increased imports, which are very expensive. Efforts to expand the region’s pipeline capacity have been blocked for years by the governors of New England’s border states – New York, New Jersey, and Pennsylvania. These moves have limited the development of the massive Marcellus shale gas resource. According to an article in The American Oil & Gas Reporter, the Marcellus shale contains over 500 trillion cubic feet of gas in place that is spread over a four-state area. Based on the history of production from the Barnett Shale in Texas, the Marcellus shale should produce conservatively 10% of the in-place resource or 50 trillion cubic feet.

In 2021, residential natural gas consumption of 4.6 trillion cubic feet, represented 17% of total U.S. consumption. The six New England states accounted for 4.5% of residential consumption. So, while natural gas is important to New England, the region is only a small part of national residential consumption. Although New England’s share of gas used in generating electricity was only 3.4%, because of the volume, the region used three times its residential consumption.

Without more pipeline capacity, the Marcellus shale resource will not be exploited. This leaves natural gas imports, primarily in the form of liquefied natural gas (LNG) as the primary supplement to pipeline gas. LNG cargoes arrive in Boston and provide peak supply during the winter. This gas comes from abroad as shipping domestic gas by water within the U.S. is restricted to Jones Act-certified vessels, of which there are none. Therefore, the LNG price is high, comparable to what Asian or European buyers pay, or 6-8 times U.S. wellhead gas prices. Generally, LNG is needed for only about 40-50 days a year, during the winter. However, cargo arrivals can be challenged by weather and scheduling.

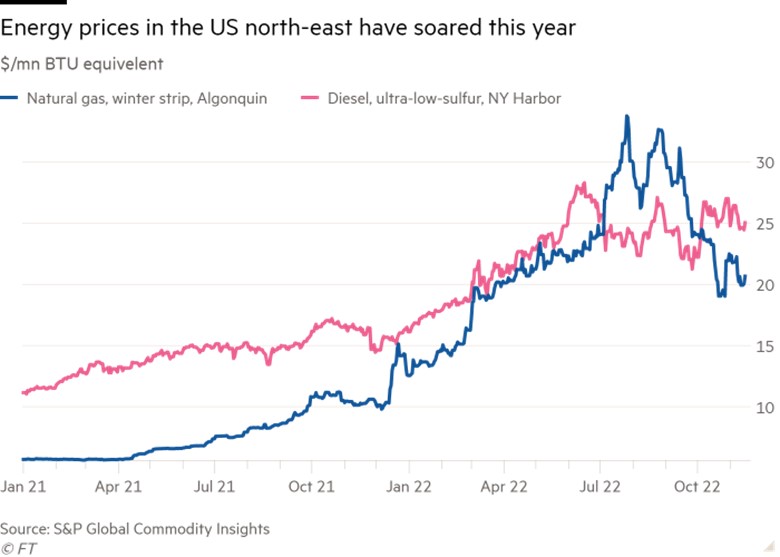

Not surprisingly, as shown in the Financial Times chart below, the price of heating oil and natural gas in New England are comparable on a dollars per million British Thermal Units basis. The chart, which covers 2021 through 2022, makes clear how the prices of heating oil and natural gas began moving higher in the fall of 2021 but took off in early 2022. Both prices have moderated in recent weeks as warm weather and reduced U.S. natural gas exports lowered domestic gas prices. Heating oil prices have also weakened as global oil prices softened with the slowing economy in response to higher interest rates and weak demand from China due to its Covid-lockdown policies that have shuttered substantial economic activity.

Exhibit 8. High Gas and Heating Oil Prices Hurt New England Consumers

Source: Financial Times

Presently, New Englanders are hoping for a mild winter to ease the cost of heating their homes and keeping the lights on. Most of the winter forecasts suggest a normal winter because of the La Niña weather phenomenon. According to the National Oceanic and Atmospheric Administration (NOAA), New England has a 40-50% chance of above-normal temperatures and an equal chance of above-, below- or near-normal precipitation. The Farmer’s Almanac 2022-23 outlook predicts that in January, the eastern half of the country may see heavy rain and snow, followed by record-breaking cold temperatures and a stormy latter half of March. Their label for the Northeast cleverly characterizes the volatility of their forecast.

Exhibit 9. New England’s Winter Weather Likely Will Be Volatile

Source: Farmers’ Almanac

On the other hand, AccuWeather senior meteorologist Paul Pastelok said while this year is the third consecutive winter influenced by La Niña, the weather setup will be more dynamic and complicated than in recent years due to other meteorological factors, like the effects of the volcanic eruption that occurred in early 2022. He concluded, “These third-year La Niñas are very tricky.”

Judah Cohen, a seasonal weather forecaster for AER, A Verisk Company, summarized the primary challenge in forecasting winter weather. The issue is how the “polar vortex,” the mass of bitterly cold weather than sits atop the North Pole, behaves. As Cohen describes the forecasting challenge, “Will we see more of that circular configuration of the polar vortex and just long periods of mild weather and lack of snowfall or are we going to get repeat incidents where the polar vortex stretches and we get kind of into these more intense periods of winter weather, cold and snow?”

Cohen went on to say, “The models kind of hinting a more of a larger stretching event, so there could be some sharp cold early on.” Despite the probability of cold outbreaks throughout the winter, Cohen’s models are suggesting a mild winter overall for temperatures during the three winter months. Precipitation should be close to normal. Cohen says his model predicts 48.3 inches of snow for Boston whose 30-year average is about 49 inches.

A mild winter would be welcomed by New Englanders, probably even by avid skiers. But a word of caution about forecasts: Buffalo’s snowstorm has already ruined many meteorologists’ forecasts for this winter for New York and the Buffalo region.

Europe’s Energy Wildcards Less Effective Than Anticipated

Forecasts for oil and natural gas prices in Europe and across the globe in the coming months are unusually unclear due to the impending imposition of a ban on the purchase of Russian crude oil by western countries starting December 5th. Additionally, there will be imposed an EU ban on purchases of Russian refined petroleum products beginning in February 2023. The difference in implementation dates reflects the EU’s concern about there being sufficient oil products refined from Russian oil available for European buyers during the coldest upcoming winter months.

The EU bans are being joined by the G7 member nations in support of Europe and especially Ukraine in its war with Russia. The petroleum ban has been implemented by some of the G7 member countries earlier. Key to this operation of this ban is that the two largest recent buyers of discounted Russian crude oil are China and India. Both countries have demonstrated no concern in buying Russian crude oil, seeing the discounted price as an economic benefit.

As part of the ban, there are prohibitions against financing, insuring, and shipping Russian oil cargos. This will make it difficult for traders and buyers of crude oil and eventually refined products to engage in the global oil trading business. But as usually happens with global markets, players find ways around restrictions. As pointed out by Amrita Sen of Energy Aspects, more oil is shipped from Indonesia than produced there. Ever hear of ship-to-ship oil transfers? Additionally, there exist financing and insuring institutions that will provide the needed support for the Russian oil trade, even if it is merely local institutions supporting local buyer purchases to help local economies.

In the case of shipping, the ban will impact the future life of any tanker that violates it. A violating ship would be prevented from ever trading in the European market during the rest of its operational life. As a result, many old tankers that were heading to retirement or were recently retired have been purchased by Russia and Russian-friendly entities to move their crude oil, recognizing that the value of these ships later will be only its scrap value. This means the global oil tanker fleet will grow but with older ships. However, with older ships, the risk of an environmental disaster from an accident grows. The irony will be if the environmentally friendly EU creates a policy that leads to environmental degradation.

Another aspect of the oil ban is that crude oil will spend more time at sea as traditional trade routes are disrupted. Christian Ingerslev, chief executive of Copenhagen-based shipping operator Maersk Tankers A/S commented, “The world’s oil-supply maps are being completely redrawn.” Tankers departing from Primorsk, Russia, which is near St. Petersburg, can reach the Dutch port of Rotterdam in roughly four days, but now many Russian shipments are being rerouted on a roughly 26-day trip around Europe, across the Mediterranean Sea, and through the Suez Canal for delivery on the western coast of India.

Replacing those Russian barrels has forced European buyers to seek oil from the Middle East, South America, and the U.S. A tanker voyage from Houston to Rotterdam is about 17 days, four times the travel time from Primorsk. Shipping executives expect that with the EU oil ban creating new trade routes, they will last. That means oil shipping costs will rise as voyages lengthen further adding to the cost of energy.

An offshoot of the oil and refined product bans is the establishment of price caps for crude oil and natural gas. The idea of implementing an oil price cap originated with Janet Yellen, the U.S. Treasury Secretary. The price cap idea is to cut Russia’s oil income, or at least prevent it from capitalizing on shortage-driven price increases, as this money is funding its war against Ukraine. As the world’s second-largest oil exporter, the rise in global oil prices since 2020 has helped bolster the Russian economy. Designing the oil price cap, though, has become a political challenge.

According to media reports, a meeting last week in Brussels among EU diplomats to establish the price cap was unsuccessful. That means they must reach a decision this week since the oil ban will start next Monday, December 5th. Reportedly, the talk about the price cap would set the price somewhere between $65 and $70 a barrel. For countries close to Ukraine, the price was too high, while for Greece and Malta with large shipping industries, the price was too low and would result in Russia cutting its exports and hurting shipping volumes. At the start of November, Russian oil was trading for $67 a barrel. At the reported price range, the cap would likely have little impact on Russian oil exports or its income.

Before this development, forecasters expected the price cap to be much lower – closer to $50, which would have been at the upper end of estimated Russian oil production costs. Analysts have been expecting the oil ban to push one million barrels a day of Russian oil supply out of the European market. They expect the Russian refined products ban in February to push another 1.4 million barrels of oil from European supplies. Potentially, Europe will need to find 2.4 million barrels of oil supply from other regions, forcing the global oil market to shift significant volumes around, which led Maersk Tanker’s Ingerslev to comment about global supply maps being redrawn. Such a shift will further raise the delivered cost of oil.

Crude oil is not the only energy market facing challenges with Europe’s plans. Natural gas on the continent is about to be subjected to a price cap to limit the soaring prices experienced earlier this year. The following chart shows just how high European gas prices got, although for only a short time.

Exhibit 10. Tracking Natural Gas Prices In Europe And The Price Cap Impact

Source: Reuters

The EU’s proposal last week would cap the gas price at €275 ($286) a megawatt-hour (MWh). However, two conditions must be met simultaneously for the cap to kick in. First, prices must remain above the threshold level for two weeks. Secondly, prices must remain €58 ($60)/MWh higher than “the LNG reference price for 10 consecutive trading days within the two weeks.”

“When these conditions are met, the Agency for the Cooperation of Energy Regulators will immediately publish a market correction notice in the Official Journal of the European Union and inform the Commission, European Securities and Markets Authority and the European Central Bank,” the EU said in its proposal. The next day after everyone was properly noticed, “orders for front-month TTF derivatives exceeding the safety price ceiling will not be accepted.”

This proposal, which must be approved by EU officials on December 19th, has numerous issues that raise serious questions about its practicality and viability. The proposal was prompted by concern about what will happen to European natural gas prices next year when it will be without Russian supplies. But this policy is planned to be put into effect in January without any rigorous testing, something seldom done by regulators. Usually, market rule changes are tested for three to four months to see what ancillary effects might occur. This proposal has already been termed “a joke” and “a non-cap” by analysts immediately after its release.

One immediate problem is that it will force traders to post much greater cash margins to protect against the possibility of the price cap being triggered. This additional burden is estimated at $33 billion, which comes after cash margins have doubled this year due to higher gas prices. Another issue is how much gas trading will be driven from the regulated exchanges to the Over The Counter (OTC) market. This means gas trading will shift from a regulated and transparent market to an opaque and private market, calling into question whether people will know the true value of gas.

As pointed out by energy writer Irina Slav, “Incidentally, the European Central Bank (one of the authorities on the reporting list for the cap, if you remember) warned against any measures that would move trades from exchanges to the OTC market.” Forcing such a market adjustment would be a move in reverse of years of pushing for openness about trading in all financial markets.

While people question the value of the gas price cap, its implementation will reflect the fear regulators and countries have about the terrible energy market Europe may face next year. This proposal, while clumsy, costly, and with unknown ramifications, maybe the best alternative regulators can conceive to avoid a free market in natural gas trading next year that comes to resemble the wild, wild, west. Possibly the December 5 oil ban will provide a test run of the gas price cap. Get ready for the potential for high oil and gas price volatility over the next few months. With unclear market price signals, what unintended market moves will happen?

Random Energy Topics And Our Thoughts

Can You Reach Net Zero By 2050?

We discovered that the Financial Times, in conjunction with Infosys, had developed a climate game for visitors to its website. The title of the game was: “Can you reach net zero by 2050? See if you can save the planet from the worst effects of climate change.” According to the website: “You need to keep global warming to 1.5C by cutting energy-related carbon dioxide emissions to net zero by 2050. In 2021, they reached a record 36bn tons a year. You must also deal with other greenhouse gases, and protect people and nature, for the planet to remain habitable.” A scare warning!

The Financial Times says the game is “based on published scientific research and bespoke modeling by the International Energy Agency.” Playing the game required responding to a series of climate and economic policy issues and potential actions. But you are fortunate to have the help of an advisor of your choosing. There are four advisors available: a teen activist sparking behavioral change; an entrepreneur developing new technologies; a businessperson influencing global leaders; and a politician driving policy change. You can make your guess about who each of these advisors is modeled after.

You are given a “budget of 100 effort points” to spend on fighting climate change and adapting to a warmer planet. The CO2 budget is 34.2 gigatons, a number that the player is trying to reduce. If you make “smart investments” in technologies or implement certain policies, you earn back points, which gives you more ammunition for actions later. If you run out of points, however, the game is over.

The game has three rounds covering different periods. The first, covering 2022-2025, asked about dealing with electricity. You were given three options: phasing out coal plants over 10-20 years with 5 effort points; letting the market work for 2 points; stopping all new coal plants globally and closing those in wealthy countries for 10 points. After making your selection, you are confronted with another policy choice dealing with transportation and electric vehicles, as well as where to invest in new technologies to curb emissions.

Depending on your choices, you can win awards for jobs, growth, nature, health, and equality, and with an award, you earn back points. The second round involved issues for the 2026-2030 timeframe, followed by 2031-2050. The policy issues deal with buildings, methane, melting glaciers, and land use. At the end of each round, you can see visually the progress made in limiting carbon emissions by sectors – electricity, buildings, transport, and industry – as well as overall.

We played the game and generally selected the more extreme policy actions to control carbon emissions. We won various awards and limited global warming to 1.444C by 2050, up from 1.2C warming as of 2020. We are not sure that many of our policy selections are realistically achievable, let alone acceptable to populations either in developed or developing countries. It was interesting that selecting the imposition of the highest carbon tax – $1,000 per ton – which added $2.30 per liter to the cost of gasoline, or $8.71 per gallon was not the preferred option. While one would have thought such a large carbon tax would be welcomed, the game warned about the political backlash it would cause. The game wanted you to select the $250 per ton carbon tax option.

Seeing the various options at each stage of the quest to reach net zero led us to appreciate that few actions can get us there without taking draconian steps such as those when economies were shut down during Covid. Such a drastic step created many more problems with long-term social and economic ramifications. So, while the Financial Times climate change game was fun, it left us convinced we must do more about mitigation and adaptation to deal with global warming than most activists realize.

New England Offshore Wind Market Declining Into Chaos

Developments in recent weeks in Massachusetts have demonstrated how challenged the U.S. offshore wind buildout effort has become. In early October, we wrote about the problems Avangrid Renewables, a subsidiary of Avangrid, an 81.5% owned subsidiary of Spanish global utility company Iberdrola, S.A. was having with two wind projects offshore Massachusetts. They are located 37 kilometers south of Martha’s Vineyard and Nantucket in the Bureau of Ocean Energy and Management lease OCS-A-534. The Park City Wind farm, an 804-megawatt (MW) project, will be joined in the offshore lease block by a 1,200 MW project called Commonwealth Wind. The power from Park City Wind has been sold to Connecticut utilities, while the Commonwealth Wind output will go to three Massachusetts power buyers.

As we noted, Avangrid held an Investor Day with analysts and investors on September 22nd. At that meeting, Avangrid Senior Vice President for Offshore Projects, Sy Oytan, revealed that the company would ask Connecticut for a “modest adjustment” to the state’s contract to purchase power from Park City Wind. In addition, Oytan said Avangrid would ask for an adjustment to the Commonwealth Wind power purchase contract with Massachusetts.

At the meeting, Oytan also indicated that both wind farms would have their respective start-up dates delayed by one year. That means Park City Wind will now start in 2027 and Commonwealth Wind would not start until 2028. The explanation for the delays is to allow more time for Avangrid to explore the new larger 17-20 MW wind turbines entering the market. The delayed start-up dates also reflect the additional time needed for environmental studies and design issues with the wind farms to secure their final permits for construction.

Avangrid initially asked the regulators to “pause” their review process for a month, giving the company time to assess the inflation and supply chain issues impacting their projects’ economics. This was less surprising for the Connecticut project since its contract was negotiated and signed in 2020. The Massachusetts project, however, was only negotiated and signed in April, merely five months earlier.

The Park City Wind power contract with Connecticut was priced at $79.83 per megawatt-hour (MWh). For customers, that price translates into 7.98 cents per kilowatt-hour (cents/kWh). However, that price only covers the cost of the power at the wind turbine and not the full cost covering gathering and transmission of the power to the grid, and certainly not the cost of backup power supplies needed for when the wind failed to blow.

Interestingly, two other offshore wind power contracts with Connecticut had been negotiated in 2018 by the partnership of Eversource/Ørstad who are building the 400 MW Revolution Wind project off the coast of Massachusetts. Three-quarters of the capacity has been contracted to Connecticut, with the initial 200 MW contracted at $99.50/MWh and the remaining 104 MWs priced at $98.43/MWh. There have been no comments from these parties about seeking an “adjustment” to their power contracts. Eversource has elected to sell all its offshore wind leases and projects given the boom underway that has developers offering obscene prices that appear to be “too good to pass up.”

The Avangrid saga has become confusing as the requests and decisions often seem inconsistent. After telling the analysts that it would seek a “price adjustment” for its power contracts, on October 20 it officially asked the Massachusetts Department of Public Utilities (DPU) to pause its review of the contracts for one month. This would allow Avangrid to attempt to renegotiate the terms of its contracts. In its filing, Avangrid wrote that absent contract changes, the Commonwealth Wind project “would not be able to move forward.”

A week later, another wind project, Mayflower Wind, a 400 MW project also under review, said it supported a pause for the same reasons. The developer wrote: “A one-month suspension would enable the parties to consider potential approaches to help ensure these offshore wind projects are economic and financeable.”

With the gauntlet thrown down, the utilities said they were not interested in renegotiating. A few days later the DPU admonished the companies for even asking to change the contracts at this late date. DPU told them they either had to commit to the power purchase agreements or pull out completely.

Mayflower Wind caved. Avangrid waited until the last minute before choosing to move forward with the project. However, Avangrid said it was not going to be able to make the numbers work with the current contract, so it asked the DPU to reconsider its renegotiation request.

In a recent interview with Commonwealth Magazine, Avangrid’s vice president for offshore wind development, Ken Kimmell, said it only required a “very modest increase” to make the project financially viable. He said Avangrid was confident its revised price would still be less than some other projects in the state, allowing it to remain one of the cheapest offshore wind farms in the country.

We are now at the “who blinks” moment. History suggests the DPU will not blink. Maybe the utilities will agree to renegotiate, but they would run the risk of angering the DPU, whose approval they still must secure. The reality is that Avangrid’s management screwed up. It only negotiated its power purchase agreements this spring – inflation, supply chain issues, and technology challenges were all well known, as were rising interest rates and overall inflation. None of this was a surprise in September. Management did a poor job of building the economic analysis which led them to underprice the contract.

Not surprisingly, the Boston national public television found numerous “energy experts” who said this spat was a “one-off” and not an indictment of offshore wind. Some of the comments were laughable and demonstrated these so-called experts do not understand the technology or the business. But as cheerleaders, they were doing their job.

At the core of the problem, other than bad management decisions, is that government subsidies for wind power are not high enough. They were set during a period of low inflation and interest rates, which everyone expected to continue. The new economic world we have entered has dramatically changed the economic parameters for projects such as expensive offshore wind. Higher interest rates upend the levelized cost of electricity calculation (LCOE). The exploding cost of the minerals needed for renewables has already resulted in the LCOEs going up when they were expected to continue to fall.

Offshore wind has many weaknesses that only become obvious when unrealistic operating and cost assumptions prove unworkable. The Massachusetts politicians are all saying they will work to find a solution – meaning figuring out how much more to stick to their fellow ratepayers. Massachusetts ratepayers are already digesting 40+% electricity rate increases starting in January, as well as warnings from the region’s grid operator of power blackouts this winter. Massachusetts power cost 26.66 cents/kWh in August, putting it third in the continental U.S. That was 67% higher than the national average.

We will be actively watching to see what pretzel-like moves all the parties will need to make to resolve this conundrum. The sad part is the ratepayers will have little knowledge of or understanding of the issues and the options for resolution. They will just be handed the bill.

The 27th Conference of the Parties under the United Nations Framework Convention on Climate Change, or COP27, ended its two-week run in Egypt’s resort town Sharm el-Sheikh on the coast of the Red Sea after going into overtime. It took two days of overtime to complete the conference’s agenda and approve a statement of action. The global climate change gabfest that drew over 45,000 delegates, political leaders, climate activists, corporate executives, fossil fuel lobbyists, members of think tanks, and the media struggled to reach the agreed-upon document that could be taken back to their governments to show their success. This document and plan of action left many climate activists upset. Maybe that is because they came to the conference ignorant of the current energy crisis and manufactured human disasters looming.

Two days before COP27 began, a group of 77 developing countries lobbied for the conference’s agenda to be revised to include a discussion of “loss and damage” payments by wealthy developed economies for climate change impacts suffered by poor countries. Otherwise known as “reparations,” the fund would be designed to compensate poor countries that suffer from extreme weather events such as droughts, floods, and heatwaves that have been made worse by the carbon emissions of rich countries. The discussion topic was approved, despite the United States and members of the European Union (EU) being in opposition to such payments. Reparations suggest legal liability, much like the lawsuits under nuisance laws brought by governments against the oil and gas industry for climate change-created damages.

In the end, a proposal by the EU to establish a fund separate from the long-standing commitment of developed economies to pay $100 billion a year to developing countries for climate aid such as the development of green energy and steps to adapt to the future climate. United States climate envoy John Kerry, who initially rejected such an idea, agreed with the EU proposal.

A committee is to be established to negotiate the structure and details of the fund and its terms for providing money to poor countries. One point about this new fund was the decision that countries such as China and India, who are eligible as developing countries for payments from the annual climate fund, would not be eligible for payments from this new fund, but rather would be asked to contribute to it, although such a step is not mandatory. It is also envisioned that a requirement for receiving money from the fund will necessitate a commitment to shut down fossil fuel use.

The new fund is planned to receive money directly from governments, but they can also satisfy their commitments through allocations of portions of their funding to quasi-governmental entities such as the World Bank.

The final conference battles were interesting. India requested changing last year’s agreement that called for a phase-down of “unabated coal” use to include a phase-down of oil and natural gas. This was an interesting development because at Glasgow last year, India forced the draft agreement language to be changed to phase-down from phase-out for coal use, something India has been increasing significantly in recent years and especially given the current global energy crisis.

India’s request, while supported by some European nations and others, was blocked by Saudi Arabia, Russia, and Nigeria. The 600 energy industry lobbyists were also seen to be working to generate opposition to the Indian proposal to the horror of climate activists. They were also upset about language proposed by Egypt regarding mitigation, which seemed to backtrack from what was adopted at COP26 and revert to language from the 2015 Paris agreement, which was before the policy emphasis shifted to limiting temperature increases to 1.5ºC rather than the earlier 2ºC mark.

In the end, not much was accomplished at COP27. Yes, a new climate fund was formed, but the details will not be known for another year. The reality of the energy crisis overwhelmed much of what could have emerged from the conference. None of that reality could overwhelm the virtue-signaling as bureaucrats and politicians hailed their commitments to fighting climate change or, in the case of U.S. President Joe Biden, he could take a bow for all the money the U.S. Congress is now shoveling toward green energy. However, just emerging is the pushback from other countries over the massive green energy subsidies to U.S. industries and companies that are creating trade battles with our allies and leading trading partners.

Contact PPHB:

1885 St. James Place, Suite 900

Houston, Texas 77056

Main Tel: (713) 621-8100

Main Fax: (713) 621-8166

www.pphb.com

Leveraging deep industry knowledge and experience, since its formation in 2003, PPHB has advised on more than 150 transactions exceeding $10 Billion in total value. PPHB advises in mergers & acquisitions, both sell-side and buy-side, raises institutional private equity and debt and offers debt and restructuring advisory services. The firm provides clients with proven investment banking partners, committed to the industry, and committed to success.